Significant features: The Fund is an actively managed portfolio of fixed interest securities. It is designed for investors who want income and diversification across a broad range of fixed interest securities and are prepared to accept some variability of returns. The Fund invests primarily in Australian dollar denominated investment grade fixed interest securities, including government securities, semi-government securities, supranational securities and credit securities and holds cash.

Investments are selected based on a range of financial, sustainable and ethical characteristics The Fund aims to allocate capital to issuers and securities that align to our sustainability themes: climate stability, human basics and innovation for good (the Sustainability Objective).

The Fund invests in securities issued by issuers that have passed Pendal’s sustainability assessment. Our sustainability assessment process is a qualitative assessment conducted at a security and issuer level. It seeks to identify issuers that, in our view, have strong sustainability credential for investment and aims to avoid issuers that we consider to have poor sustainability outcomes.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Bloomberg AusBond Composite 0+ Yr Index by 0.75% p.a. over rolling 3 year periods.

What can investors do when bonds stop performing how they’re supposed to in portfolios? Pendal’s Vimal Gor has been thinking about this – and has some answers

- Use tested strategies to achieve diversification and yield

- Alternative duration is a new way of thinking about asset allocation

- Find out more about Pendal’s fixed interest strategies

What can investment managers do when key attributes of bond investing — yield, diversification from equities — are low, asks Pendal’s Vimal Gor.

“You take market factors that already exist … and build a new asset allocation process around them,” says Vimal, who has pioneered “alternative duration” investing in Australia for several years.

The idea is to identify factors in different trading environments — such as momentum, volatility, skew (which involves the implied volatility of options) — and use a strategy that takes advantages of these factors to achieve desired outcomes.

“We think the uptake of this sort of alternative duration thinking is going to be very material in the next few years,” says Vimal, who recently began specialising in this space.

A five-person team, headed up by Vimal, is focused on bringing new thinking and new opportunities to income clients.

(Vimal was previously head of Pendal’s Income and Fixed Interest team — then known as Bond, Income and Defensive Strategies).

Investors can consider alternatives to the bond market to achieve the attributes they want in their portfolios, says Gor. That means thinking about alternative duration.

Duration in fixed income markets is a measure of the sensitivity of the price of a bond to changes in interest rates.

“Global government bonds have been in a long-term bull market for 30 years. Yields have fallen as nominal GDP and inflation has fallen.

Find out about

Pendal’s Income and Fixed Interest funds

“Ultimately, as global government bonds approach zero, the efficiency and effectiveness of fixed income as a diversifier to equities in a portfolio is dampened because they have less negative correlation to equities in a time of stress, and that’s one of the main reasons you want global bonds.

New way of thinking

Three years ago, Pendal embarked on a project to better understand how to achieve the attributes that global government bonds traditionally performed, including diversification.

“How do we approach the asset allocation problem when government bonds aren’t as useful as the used to be?”

Gor and his team’s approach was to rethink what the post-Covid economic and market environment was like.

“It’s a new way of thinking about asset allocation. We took market factors that already exist … and built a new asset allocation process around them.”

That meant identifying factors in different trading environments – momentum, volatility, skew (which involves the implied volatility of options) – and using a strategy that takes advantages of those factors to achieve desired outcomes.

“For example, intraday momentum is a systematic strategy that works very well in periods of drawdowns. Foreign exchange carry works very well in periods when equity markets are going up.

“By identifying these factors, and their risk-return characteristics, we are able to blend them in a portfolio to get a specific outcome.”

Traditionally, investors approach portfolio construction by blending assets to achieve a 60 per cent growth assets, 40 per cent defensive assets, for example. That mix determines what an investor’s profile is.

“We are coming at it from looking at what outcome profile would we like, and how do we get there by bolting together these factors which have very long track records. It’s a very different way of approaching asset allocation.

“We use strategies based on different factors in the multi-asset markets and apply and change them as we go through the cycle, depending on the environment.”

About Vimal Gor and Pendal’s Alternative Duration boutique investment team

Vimal Gor is Pendal’s Head of Alternative Duration.

Vimal’s new five-person team focuses on bringing new thinking and new opportunities to income clients.

Vimal was previously head of Pendal’s Income and Fixed Interest (I&FI) team (formerly known as Bond, Income and Defensive Strategies). Pendal I&FI is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Significant Features: The Pendal Focus Australian Share Fund is an actively managed concentrated portfolio of Australian shares.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that significantly exceeds the S&P/ASX 300 (TR) Index over the medium to long term.

Here are the main factors driving the ASX this week according to portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams

RECENT trends persisted last week, although news flow was relatively quiet.

US and Australian 10-year government bond yields rose 15bps for the week, prompting further rotation from long-duration growth plays.

Commodity prices continued their climb. Brent crude oil rose 3.9% and copper 2.1%. There was some relief for iron ore, which gained 9.7% after recent plunges.

Gas and electricity prices continue to surge in the US, the EU and Asia. They are at record levels in the UK and EU, while volumes in storage are materially below historical averages. Moscow stepped in late last week, saying it was prepared to take steps to calm energy markets.

US payrolls data on Friday asked more questions than it answered in terms of the pace of tapering and rate rises.

The S&P/ASX 300 gained 1.86% and the S&P 500 0.83%.

Covid outlook

New case numbers continue to improve in US and most places around the world.

Singapore is an outlier, walking back some re-opening measures after a material resurgence in cases.

Severity of infection is proving far lower in vaccinated people. About 98% of recent Covid cases experienced either no symptoms — or only mild effects — in the 28 days before becoming positive.

Pfizer has asked the FDA to approve the vaccine for 5-to-11-year-olds. The FDA took about 30 days to approve the Pfizer vaccine for 12-to-15-year-olds.

Israel last week became the first country to effectively make vaccine boosters mandatory.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Six months after a second vaccine dose, Israelis now require a third dose to retain a fully immunised “green pass” allowing entry into restaurants, gyms and other venues.

Over the past two months Israel has provided boosters to 39% of its population, significantly ahead of all other countries.

The case count there has been pushed down by 54% over the past two weeks. Health outcomes appear materially better than for those with just two doses.

Economics: US outlook

Friday’s US employment had been eagerly awaited for some read-through to Fed policy. But there was not enough clarity to read one way or the other.

There were expectations that September non-farm payrolls would see a material rebound given a reduction in unemployment benefits, the return to school after summer break and continued vaccinations.

But the headline came in weaker than expected with 194,000 jobs added versus consensus expectations of 500,000.

That said, the previous two months were revised up by 169,000 jobs. There was also a distortion from government jobs, which have been volatile and fell by 123,000.

Private payrolls were up 317,000 month-on-month. Hiring in tech-related service sectors remained strong. Leisure and hospitality was less buoyant (up 74,000) reflecting difficulties in recruitment.

The question is whether this meets the definition of “decent” economic momentum Powell flagged in September to keep tapering on track.

A key point of debate remains around the extent to which displaced workers are retiring or re-training rather than returning to old jobs.

Earlier explanations for lack of labour — such as the effect of benefits or the summer break — seem to be falling by the wayside.

The jobless rate fell to 4.76%, down from 5.2%. The modest pace of hiring will be enough to push the US towards full employment, since the labour force participation rate for prime-aged workers fell.

Average hourly earnings rose 0.62% month-on-month, ahead of a 0.4% expectation. The means the question of the Fed needing to tighten sooner rather than later remains live, although a mix shift of more growth in lower-paid hospitality jobs may see wage growth ease going forward.

Economics: Australia and New Zealand

The RBA left policy settings unchanged, as expected, including the cash rate target, the 2024 yield target and the pace of Quantitative Easing purchases.

The RBA maintained its positive medium-term view while noting ongoing disruptions from lockdowns in Sydney and Melbourne.

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

The RBNZ lifted its official cash rate by 25bp to 0.5%, also in line with expectations. It maintained a moderate, hawkish bias, noting that “further removal of monetary policy stimulus is expected over time”.

APRA announced an increase in the minimum serviceability buffer of 0.5% (from 2.5% to 3%) The market had generally expected APRA would wait until early 2022. Clearly regulators appear more concerned about risks in the housing market than anticipated.

The message is that while banks are “well capitalised and lending standards have generally remained sound”, action is being taken to offset the “heightened risks for the financial system from lending at very high levels of indebtedness”.

Basically regulators are worried about households taking on too much debt relative to incomes at a time of record low rates. The increase in serviceability buffers will be effective from the end October.

Elsewhere, business surveys and consumer sentiment survey results have fallen as a result of lockdowns, but importantly they remain high compared to pre-Covid levels.

Markets

Bond yields rose materially last week. Commodity prices also rose which, in combination, underpinned a continued rotation away from growth.

A rebound in iron ore provided some much-needed respite for the major miners.

Energy (+4.49%) and Financials (+3.27%) did best, while Health Care (-0.26%) and Technology (+0.25%) lagged.

Worley (WOR, +9.8%), AGL (+7.9%), Woodside (WPL, +6.7%), Origin (ORG, +6.5%), Santos (STO, +6.0%) and Oil Search (OSH, +5.37%) all had a strong week as energy prices continued to climb. The oil price benefited from news that the US are unlikely to tap strategic fuel reserves.

Higher bond yields supported the financials, particularly QBE (QBE, +8.1%), IAG (IAG, +6.8%) and Challenger (CGF, +5.4%).

Insurers had good news with a federal court ruling that was largely in their favour in the second test case for Business Interruption (BI) related claims from Covid.

The outcome was seen as more commercial-friendly then consumer-friendly, which differs from many judgements globally. An appeal is set down for November 21 with further clarity expected on December 21.

About Jim Taylor and Pendal Focus Australian Share Fund

Drawing on more than 25 years of experience investing in top-performing Australian companies and a background in accounting, Jim manages our Long/ Short Fund and co-manages our Imputation Fund. He is a Chartered Accountant with membership of the Australian Institute of Chartered Accountants.

Pendal Focus Australian Share Fund has beaten its benchmark in 12 years of its 16-year history (after fees), across a range of market conditions. Find out more about Pendal Focus Australian Share Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

As Australia embarks on take two of the post-covid re-opening sequence, focus is turning to reducing risk in our overheated housing market. ANNA HONG explains

IN A MOVE that surprised no one, Australia’s financial system regulator APRA took steps to cool the housing market on Wednesday.

The decision to tackle house prices with macro-prudential instead of monetary tools reflects the reality that we are still in a tentative economic situation despite rocketing house prices.

This week Australia edged towards take two of the post-covid, re-opening sequence.

NSW firmed up its re-opening date of October 11. Victoria pushed forward with a roadmap out of lockdown despite rising case numbers.

We are opening up just in time to face global supply chain issues that are already creating havoc — and may worsen with potential delivery strikes.

Against this backdrop of uncertainty, RBA governor Phil Lowe reiterated the central bank’s dovish stance earlier in the week.

His main objective was to reduce unemployment and boost wages and prices.

That leaves APRA with the heavy lifting on cooling the housing market.

Property obsession

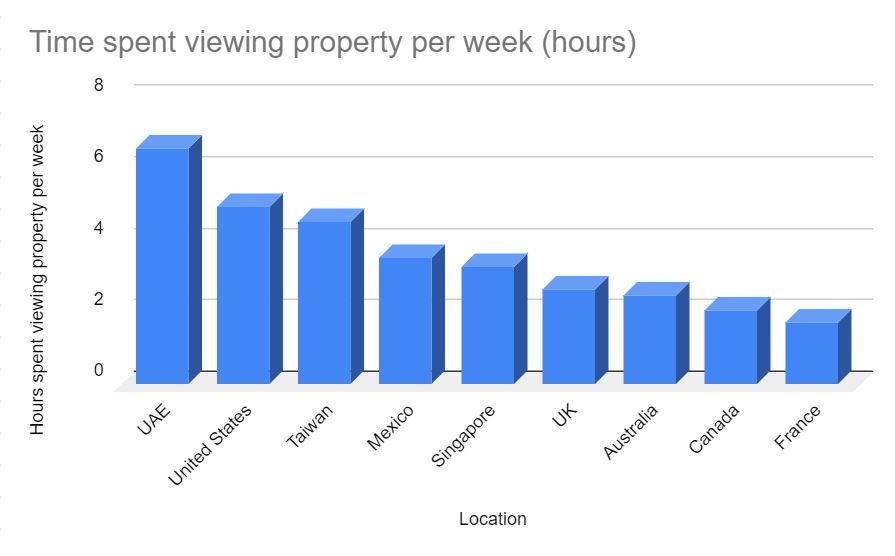

Australia’s obsession with property certainly isn’t new.

We spend an average of 2.5 hours a week researching property — even when we’re not in the market, according to HSBC data from 2019:

That’s twice the time spent at the gym (1.08 hours) and three times as much as we talk to our parents (0.88 hours).

Under such benign housing credit conditions — low rates, greater certainty on repayments with the fixing of rates thanks to the Term Funding Facility, lockdowns coupled with income from JobKeeper — it’s not surprising that we’re ploughing money into property.

On Wednesday APRA sent a letter to the banks, instructing them to increase the minimum interest rate buffer applied to new home loan applications.

The serviceability buffer will increase from 2.5 per cent to 3 per cent.

“While the banking system is well capitalised and lending standards overall have held up, increases in the share of heavily indebted borrowers, and leverage in the household sector more broadly, mean that medium-term risks to financial stability are building,” said APRA chairman Wayne Byres.

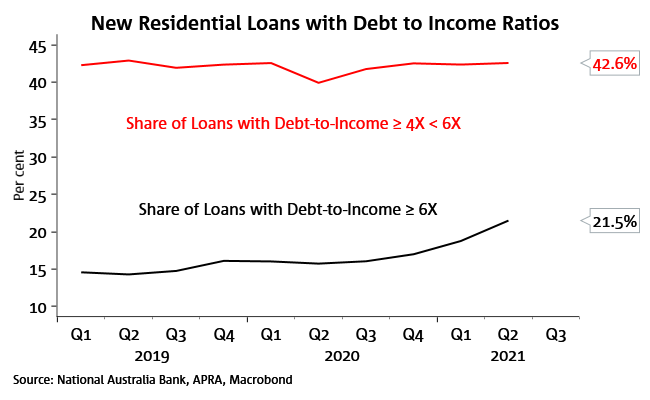

APRA wants to reduce maximum borrowing capacity, since a fifth of new loans now have more than a 6:1 ratio of debt-to-income, as this NAB chart shows:

The implications

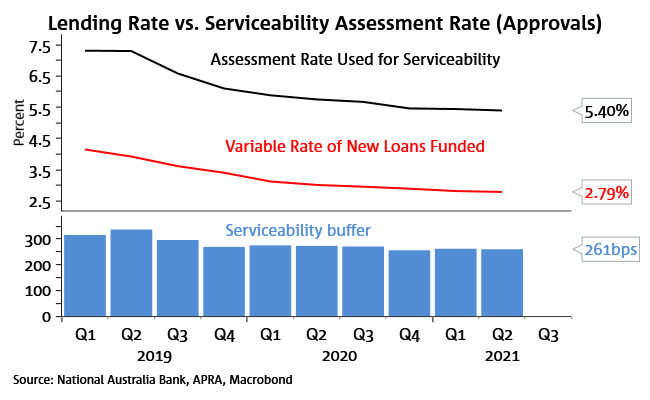

This increase in serviceability buffer reduces the borrowing capacity of borrowers by 5 to 6 per cent, again shown in this NAB chart:

Only time will tell if the latest measures put a dent in the housing market.

History has shown these may be mere bumps in the road instead of a large-scale correction.

But it’s just the first shot across the bow from APRA.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Some Chinese stocks are looking good value. But you need to think differently about value investing in emerging markets explains PAUL WIMBORNE

- Important catalysts to realise value are missing in China

- Value in emerging markets should be assessed differently

- Find out about Pendal Global Emerging Markets Opportunities fund

ARE Chinese stocks good value?

“It’s a question we’re getting asked by a lot of clients,” says Pendal’s Paul Wimborne.

The MSCI China index has halved since its peak in February 2021. Falls of that magnitude in developed markets soon attract bargain hunting buyers that sow the seeds of the next bull market.

But does the same thesis hold for China?

“The answer to that question at the moment is no,” says Wimborne, co-manager of Pendal Global Emerging Market Opportunities Fund.

“The reason for that is we think value in emerging markets should be assessed very differently than in the developed world.”

A value stock is one that trades at an attractive price relative to fundamentals like its earnings, dividends or assets.

Many Chinese stocks appear to fit the bill, including internet leader Alibaba and telecommunications giant China Mobile.

Both are trading at single-digit price earnings ratios with strong balance sheets and good quality earnings.

Find out about

Pendal Global Emerging Markets Opportunities Fund

But the appearance of value is only part of the investment story, says Wimborne says. Investors also need to be able to realise that value.

Three catalysts for realising value

“In the developed world, you have three strong catalysts for the realisation of shareholder value:

- Strong corporate governance

- Minority shareholder rights, and

- Entrenched culture of merger and acquisition activity

“These catalysts ensure the realisation of value when a company’s shares are not doing well.

“In the emerging world, we think these catalysts are often lacking.”

Alibaba — once a popular and strongly performing stock for western investors — is a prime example of how value can be illusive, says Wimborne.

“For starters, foreign entities are not allowed to own Chinese internet businesses, so Alibaba has to have this strange ownership structure — a variable interest entity, where shareholders have economic but not legal control.

“Management can decide what they want to do with the business and minority shareholders have no way of exerting any control or influence over what management does with free cash flow.

“The business throws off a lot of free cash flow, but we struggle to see how minorities will actually get hold of any of it.”

This is exacerbated by China’s closed capital account that stops money moving freely in and out of the country.

Adviser Louise is invested

in making our world

A better place.

Louise meets a woman who

turned her life around thanks

to responsible investing

“Alibaba would need the permission of the Chinese government to be able to send that money offshore to foreign shareholders.

“We think it’s extremely unlikely that the Chinese government would approve significant dividend payments that would catalyse value for Alibaba.”

Wimborne says these concerns hold true for other emerging markets as well.

Take care in South Korea

“South Korea is another example where value has not worked well.

“Corporate governance is not well entrenched in South Korea.

“The family-run chaebol industrial conglomerates have had little consideration for other stakeholders — such as minority shareholders — in order to develop the economy over the past 60 or 70 years.

“It’s starting to improve at the margin, but minorities do not get treated as well as they should, relative to developed markets. As a result Korea trades at big discount to other emerging markets.”

Investors in emerging markets need to be aware of these kinds of local specifics and not simply apply western ideas to developing countries.

“The way we run our portfolios is very top-down, country-specific — looking at the country’s history, its economic outlook and its equity culture to determine where we think the potential returns will come from.

“Part of that is assessing each country’s corporate governance, its treatment of minority shareholders in general, and the culture of rewarding equity holders.”

About Paul Wimborne and Pendal Global Emerging Markets Opportunities Fund

Paul Wimborne is a senior portfolio manager of Pendal’s Global Emerging Markets Opportunities Fund with James Syme and Ada Chan.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.