Warren Buffett’s “economic moat” isn’t what it used to be. Investors need to ask new questions about competitive advantage, says Pendal Asian Share Fund manager SAMIR MEHTA

- Old competitive advantages may no longer apply

- Outsourcing, globalisation now a weakness

- Find out about Samir’s Pendal Asian Share Fund

WARREN Buffet popularised the idea of the “economic moat” to describe a company’s competitive advantages.

But with geopolitical conflict, government sanctions, supply chain disruptions and a new sweeping deglobalisation, companies’ economic moats are not what they once were, says Samir Mehta, who manages Pendal Asian Share Fund.

“The years of seamless globalisation are behind us,” says Mehta.

“Disparate systems with built-in redundancies mean higher costs of doing business going forward.

“It is prudent is to assume lower profit margins and much lower returns on capital for most businesses.

“We might need to reassess what we pay for businesses once thought secure due to their moats.”

Rethink competitive advantage

Sustainable competitive advantage has taken many forms — it could be the ability to produce goods cheaper due to sophisticated outsourcing arrangements, the ability to source low-cost raw materials, or access to less-expensive labour.

“But in a deglobalised world where supply chains are disrupted and sanction risk is real, new questions need to be asked,” says Mehta.

“Where are your email servers based? Which cloud computing software do you use?

“Are you dependent on Visa, MasterCard or Amex for your corporate credit cards?”

Some of the fundamental technologies that investors take for granted have geopolitical connections that can make companies that rely on them vulnerable, says Mehta.

The US government owns the GPS (global positioning system) which powers location-based services like maps on smart phones. American and European banks control the SWIFT international payments system.

Find out about

Pendal Asian Share Fund

“These are all things which we just take for granted,” he says.

Mehta says the end of the era of just traditional economic moats is another example of change in some of the core factors that investors have taken for granted for decades.

“These are cyclical changes in a long business cycle,” he says. “From the 1980s, we witnessed falling interest rates and lower inflation – but at some point in time, we know that this economic cycle will likely turn.”

Mehta says investors should look to the past to gain insights into what the new world might look like.

“Cycles last decades; we’ve had many instances in the past where we’ve lived in inflationary environments or seen changes in the way economies are managed.”

He recalls the changes Asian economies went through after the crisis of 1997/98 as the International Monetary Fund and western governments imposed sweeping change across the way economies were managed in return for bailouts.

Look for new clues

With some of the basics of investing under threat, Mehta says investors need to look for new clues to find success over the next decades.

One particularly important change is to watch for the effects of the re-engagement of government in economies.

This is typified by Beijing’s deep intervention into Chinese business to reduce inequalities and help contain cost of living pressures, but it is also noticeable in the west as governments deepen their involvement post-pandemic.

Mehta says this re-engagement of government is something of a return to the past for some Asian economies, where the state has a history of “managed capitalism” and favouritism in service of advancing national goals.

“In the past we looked for markers such as higher returns on capital from competitive advantages, but now I have to reorient myself – are there companies that derive their moats from protectionism?

“Where are the companies that will benefit because a government wants them to benefit? “You have to think hard and reassess the level of vulnerability for companies. In that sense, we are heading back to the future.”

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Coping with volatility is normal for investors. Here are a few timeworn tips from Pendal’s Asian Equities Fund manager SAMIR MEHTA

- Diversification key to coping with volatility

- Sell-offs can bring opportunities

- Find out about Samir Mehta’s Pendal Asian Share Fund

INFLATION energy prices, interest rates, and now war in Europe: at times it feels like there is nowhere for investors to hide.

Yet coping with volatility and uncertainty is situation normal for experienced investors, who can turn to a few tried and trusted tips to get them through the downturn, says Pendal’s Samir Mehta.

“There are periods of time a portfolio will struggle,” says Mehta, who manages Pendal Asian Shares Fund.

“The cause of volatility and sell-off is global in nature — no geography and very few sectors have been spared.”

Investors can turn to three timeworn strategies when seeking to cope with market uncertainty, Mehta says.

Diversify

First, he says check that your portfolio is appropriately diversified. Even in times of market dislocation, different assets perform differently.

Past few months, the best performers were in the energy sector (oil, gas and coal producers) and miners. A properly diversified portfolio has exposure to these sectors.

This will test ideological convictions, says Mehta.

“But the goal is to identify a few of these areas of strength and have a bit of exposure — even if they are areas where normally you don’t want to participate.”

Find out about

Pendal Asian Share Fund

Diversification includes holding an allocation to cash through the turmoil.

“You need to try to preserve as much capital as possible,” he says.

Bunker down

Second, Mehta says investors should bunker down and wait out the volatility.

“Sometimes you have to just live through these painful periods of underperformance,” he says.

Look for opportunity

And finally, he says it is a good time to look for opportunities to change the portfolio as the price of companies becomes divorced from their fundamentals.

“Sometimes, the selling is indiscriminate,” says Mehta.

Mehta says broad-based market sell offs often throw up opportunities to buy companies at attractive prices.

“To navigate through this, I try to identify companies that will come through this in a much better state than they are today.”

Case study: Meituan

He uses the example of a company in his portfolio, China’s food delivery giant Meituan.

Meituan has been sold off amid concern it could suffer from Beijing’s regulatory actions aimed at improving equality and alleviating cost of living pressures for Chinese families.

“But they are a business that in my view benefits the community – they provide a lot of employment. Their fees for restaurants are among the lowest in the world. And they are very profitable,” he says.

Mehta’s advice: “Be careful not to the use the price of a company to judge its value.”

“These are the decisions that investors have to make with the kind of confluence of events that are taking place.

“Whether it’s geopolitics, Federal Reserve action, Chinese regulatory issues or inflationary pressures — we have to look through this fog and try to understand which are the businesses that genuinely will come through these problems.”

“The unintended consequences of actions in this war will play out over a long while to come. War teaches us why geography matters and why history can’t be ignored.

“No one felt the weight of his actions than the so-called father of the atomic bomb, J. Robert Oppenheimer (as you can see in this video below).

It’s a sober realism worth listening to.

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

As a sharp downturn in world markets shakes confidence, investors should look to the past to identify a path through volatility, says Pendal Group’s Asian Share Fund manager SAMIR MEHTA

- Volatility in 2022 is following a familiar pattern

- Think ‘VEPL’: Valuations, Earnings Progression and Liquidity

- Find out about Samir Mehta’s Pendal Asian Share Fund

“HODL!” has been the call to arms for a new generation of investors in recent years — an accidental misspelling of “hold” that became a meme and a rallying cry for how crypto investors should behave when faced with market turbulence.

But as a sharp downturn in world markets so far in 2022 shakes confidence, perhaps investors need to adopt a different meme, says Samir Mehta, who manages Pendal’s Asian Share Fund.

“The meme we should be guided by is VEPL! — Valuations, Earnings Progression and Liquidity,” he says.

Market volatility so far in 2022 is showing a familiar pattern to previous downturns and investors can look to the past for a path through, says Mehta.

He recalls a market aphorism that as the tide turns on easy monetary policy. It’s the small fish that die first as those asset prices underpinned by excess liquidity and leverage start to unwind — but ultimately at some point “a whale gets beached”.

This time around, examples of the ‘small fish’ are the collapse in the Turkish lira amid runaway inflation and the rapid retreat of cryptocurrencies.

“We now have to figure out — where is the whale?” says Mehta.

Past ‘whales’ have been the collapse of the US housing market in the GFC, the tech wreck of 2000 and the Asian financial crisis of 1997.

Find out about

Pendal Asian Share Fund

‘Every generation thinks they invented sex’

Mehta recalls a decade ago launching the Asian Share Fund with a presentation titled ‘Every generation thinks they invented sex’.

Little has changed with the latest generation of investors, he says.

“This ‘everything rally’ in 2020 and 2021 was premised on shiny new memes and radical technological blockchain breakthroughs. A new paradigm. Yet what has not changed is human greed and fear.

“Excesses, once created, usually deflate over time.”

Mehta says that, as a result, the key skill for investors in 2022 is going to be patience.

“As of now, it would be foolhardy on my part to opine with confidence that this sell off in January in the US is start of a prolonged bear market.

“[But] the confidence that I do have is to suggest that prudence dictates diversification away from momentum-oriented assets.”

So where should investors turn in 2022?

Mehta says he is becoming more optimistic on the outlook for China and intends to increase portfolio weighting over the course of the year.

While market sentiment towards China is negative, it will be one of the few countries loosening monetary policy in 2022.

“In my view, monetary policy will loosen faster than most expect in China,” he says.

Shares in southeast Asia also remain cheap and out of favour, says Mehta.

“That is why I kept adding to our holdings in that region. I still remain convinced that patience in those names will help us in 2022.”

Mehta says the southeast Asian region — with significant stock markets in Singapore, Thailand, the Philippines, Malaysia and Indonesia — has historically been vulnerable to external shocks, “but today that is all relative”.

Elsewhere, valuations for Indian stocks in 2022 will likely face the headwind of higher oil prices but strong competitive dynamics in many industries by dominant firms is an attraction.

“Ultimately, the test as always is whether the stock I own manages to deliver on earnings.”

And how about that whale?

Mehta suggests investors watch three asset classes for signs of trouble: the Chinese property market, the euro, and the private equity and venture capital sector.

“I am not a macro-economist and I have been wrong before, but I’m trying to look back through history and identify where today’s biggest vulnerabilities may lie,” he says.

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Omicron is adding uncertainty to investing at the moment. Here Pendal portfolio manager Samir Mehta discusses how to approach investing in periods of doubt

- Investors face weeks of uncertainty with Omicron

- Barbell strategy a way of approaching investment uncertainty

- Find out about Samir Mehta’s Pendal Asian Share Fund

INVESTORS expect weeks of uncertainty as lab technicians probe the Omicron variant.

How to tailor portfolio construction in such times?

It is an apt question in a week where unexpected Covid variants have roiled markets. But the important thing to remember is that uncertainty has always been a feature of investing, says Samir Mehta, who manages Pendal Asian Share Fund.

It’s not just the big unforeseen events that are difficult to predict, he says.

Mehta points to records of Treasury bond yield forecasts from the Society of Professional Forecasters — the oldest quarterly survey of macroeconomic forecasts in the United States conducted by the Federal Reserve Bank of Philadelphia.

Year in, year out for the past two decades, America’s top economists have predicted that bond yields will rise.

As you can see below from this analysis by Bianco Research, year in, year out they have been by-and-large wrong.

Bond bearishness has been a constant for decades, and horribly wrong for decades. pic.twitter.com/noSV4aN23r

— Jim Bianco biancoresearch.eth (@biancoresearch) November 19, 2021

“Humans by nature — especially in our industry — need to appear knowledgeable. And to appear knowledgeable you have to come across as if you know a few things,” says Mehta.

“At the moment, it seems like the rational thing to do is to consider the possibility of interest rates going up because that’s what everyone is saying.

“But there have been so many instances where we’ve been in similar positions like this, and the forecasts have been consistent for rising rates, and they just have not panned out as expected.

“There’s this big tug of war and I have no clue as to which way it will go.”

How to manage uncertainty

So, what do you do when you don’t know what will happen next?

“The question is how do you make decisions in an uncertain environment,” says Mehta.

“And that’s the job. Not just for people like myself, but so many professions involve decision making under uncertainty.”

Mehta says a simple way to construct a portfolio in uncertain times is to use a “barbell strategy” where a portfolio is weighted to opposing outcomes.

“If you do not have conviction on outcomes, you want to hedge your bets. That’s what a barbell is,” he says.

Find out about

Pendal Asian Share Fund

“You have enough on both sides so that you don’t get caught on the wrong end of either of them and as evidence start to accumulate, and you get more conviction, you move towards where the evidence is taking you.”

Mehta says the biggest unknown in markets remains whether inflationary pressures are transitory or here to stay.

“Let’s say the forecasters are right, that inflation is likely to be trenchant and not transient.

“That means 10-year bond yields and interest rates around the world have to rise.

“The question becomes which countries, sectors and companies are likely to be uncorrelated to the effects of rising inflation and rising interest rates?

Investing in Asia

Mehta says investors could look to Southeast Asia for this exposure.

“Southeast Asia is neglected, completely out of favour and cheap. But countries like Indonesia and even the Philippines are benefiting from the reflation due to commodities.”

And China should also be back on the list in a barbell approach.

“China is completely out of favour — but it is the one country that has acted diametrically opposite from all others from a central bank action perspective.

“The People’s Bank of China has tightened monetary policy, not allowed lending to get out of hand, the property bubble is coming under strain, GDP growth is affected.

“If the Western world goes into a rising interest rate, rising inflation environment, could we anticipate China doing the opposite? Should we be alive to the fact that liquidity conditions in China could start to become benign at a time when the rest of the world is quite negative on China?”

And what’s on the other side of the barbell?

Here, Mehta says a well-structured portfolio should own the companies that will continue to thrive should inflation prove transitory.

“I want to have some part of my portfolio in structural winners and growth in case forecasts of rising interest rates based on rising inflation turns out to be wrong.”

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

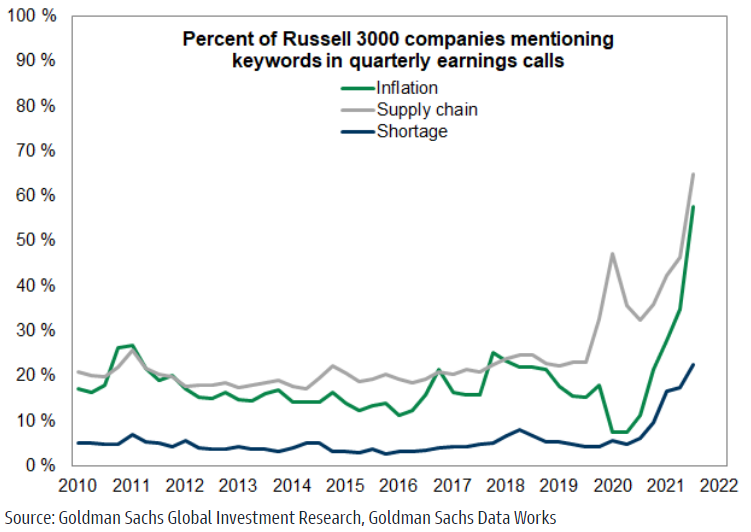

Equities investors will see a continued impact from rising energies, but talk of a new energy crisis is overblown says Pendal’s Asian equities expert SAMIR MEHTA

RISING energy prices are posing an increasing threat to the global economic recovery, with very few businesses immune from the ripple effects of a higher oil and gas prices, according to Pendal portfolio manager Samir Mehta.

Mehta, who manages Pendal Asian Share Fund, says the effects of higher oil and gas prices mean lower disposable incomes across developing and developed markets — and will crimp business profits as the world emerges from Covid.

But talk of a new energy crisis is overblown, he says. The world is in a very different place from the last oil shock in 2008, with materially higher incomes and more accommodative policy to soften the direct blow to incomes.

“You also have to consider the time value of money. The last time the oil price went above $100 was 2008. A dollar does not have the same value today as it did in 2008.

“Headline prices have increased significantly this year, however in a historical context there are substantial differences.

“Global GDP has grown by roughly 3 to 4 per cent per annum over the past decade.

“Relative to GDP, energy prices are still benign compared to 2008.”

A headwind for economic recovery

Still, rising energy prices are coming at a delicate time for global markets, which are also coping with a slowing Chinese economy, supply chain-related inflation and a gradual tapering in monetary policy stimulus as bond-buying programs shrink relative to the size of the economy.

Find out about

Pendal Asian Share Fund

“In India, petrol and diesel prices are above all-time highs,” says Mehta.

“Americans are starting to feel it at the pump. Australia and every other country are going to face the same problem.”

The underlying driver of higher energy prices is restrictions on supply due to underinvestment in energy infrastructure as the world grapples with carbon emissions reductions targets, says Mehta.

China recently ordered coal mines back to production after sweeping power cuts aimed at improving environmental outcomes.

China’s reaction to energy shortages is also likely to include limits on coal prices and coal company profits to push energy costs lower.

But this heavy-handed approach is likely to have unintended consequences, says Mehta.

“There is a clearing mechanism in capitalism called pricing which usually brings supply and demand into some kind of equilibrium.”

“Markets are telling us we need more supply. But as a society are we prepared to allow more coal or oil or gas production?”

China’s zeal for zero-COVID ahead of the Beijing Winter Olympics is also complicating the outlook, with ports, transport, cities and even whole provinces at risk of shutdowns if COVID cases emerge.

“They are the last hold-outs,” says Mehta. “Every other country except North Korea has given up on zero COVID – even Australia and New Zealand.”

Businesses face a conundrum

The result is that businesses — and investors — are faced with a difficult conundrum.

“I may own a business that has navigated supply chain problems, but all of sudden my customers might face lower disposable incomes,” says Mehta.

“Or I own a business in which disposable incomes are not a problem – the business has pricing power – but that business can’t meet demand due to lack of inputs as their suppliers are struggling.

“Purchasing managers at companies must be ‘over ordering’ to hedge their bets and build contingency reserves — this could mean an inventory build-up. Strong current demand might not necessarily mean end consumer demand. There are several issues to grapple with.”

Idiosyncratic investor risks

So, how can investors proceed through such an uncertain outlook?

Mehta advises a stock-by-stock and country-by-country approach but is still subject to risks.

“This is a situation in which few businesses – if any – will remain immune from the conditions we find ourselves in,” he says.

“Almost every single company in their result announcements mention rising costs.

“The intensity of uncertainty has increased.

“We are likely facing a very volatile period for markets with idiosyncratic risks – be prepared for it.”

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Fading government stimulus is placing global stock markets at a turning point and investors should reassess risk, says Pendal’s Samir Mehta

FADING fiscal stimulus and the dwindling effect of central banks bond purchases is placing global stock markets in a precarious position — which means it’s time to reassess portfolio risk settings, says Pendal’s Samir Mehta.

Mehta, who manages Pendal Asian Share Fund, says the fact that central bank bond purchases are being held at absolute dollar levels means they are not keeping pace with growing money supply in the economy.

That’s ahead of any formal tapering of stimulus and comes while business and consumers are also facing headwinds from supply constraints and rising prices.

It’s time for a change in investor mindset from the strong growth of 2020 to consider a period where stockmarket returns may be more subdued and risks are increasing, says Mehta.

“Policy has now become restrictive, even though it is loose relative to 2020,” he says. “What you want to do now is to reassess the risk.

“If you find you have too much weighting in an asset class that has done exceedingly well — and I’m pointing to developed markets like the US and particularly the technology names — you should be thinking of rebalancing.”

Take a big-picture view

Mehta says investors should take a big picture view of what’s been driving markets over the past two years to understand where they might go next.

“Even though I focus on picking the right stocks with a bottom-up approach to portfolios, at times like this you need to sit back and revaluate overall risks.”

For much of 2020, stock markets roared as governments allowed deficits to run to combat the pandemic and central banks reduced interest rates to zero or below.

Find out about

Pendal Asian Share Fund

Stimulus droves household disposable incomes higher. Coupled with debt relief from lower interest rates, rental stays and mortgage relief, spending boomed.

Business bottom lines also benefited from the pandemic. Discretionary costs such as travel were slashed. Many took the opportunity to get structural costs under control and commodity price falls lowered input costs.

“Profit margins for the corporate sector went up — profit growth was staggering,” says Mehta. “That was 2020.”

Now the world looks different.

Three truths that drive markets

“There are three universal truths that drive markets,” says Mehta.

“One is earnings progression — are earnings going up or down? Two is valuation — is that asset you want to buy cheap or fair value or expensive?

“And third — is there enough liquidity to support that asset?”

On those three measures, global investing is looking risky, says Mehta.

“Last year you had disinflation or deflation — this year you have inflation, which is a creeping tax on consumers.

“But from a corporate perspective, it’s also a problem as energy and commodity prices rise, which is increasing raw material prices.

“So even though demand may be strong, supply may be constrained.”

The change is akin to a shift away from the winners of last year in favour of the companies that did it tough during the pandemic, he says.

“It is rearranging the deckchairs of corporate profitability across the world — profits are moving from companies that made lots last year to those that were starved of it.

“So the logistics companies and the container-shipping companies are now making money hand over fist.

“Similarly, commodities — last year they were a loser, this year are a winner.

“When I put all of this together, we are at a juncture in markets where it’s now likely that even though demand conditions are good, even though consumer balance sheets are good, even though income levels are good, there are pockets of resistance on the horizon.”

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Ongoing supply constraints will likely see 2.5% inflation in Australia next year. That may mean the start of a modest rate hiking cycle in 2023, says Pendal’s Tim Hext

INVESTORS were hoping the things driving risk markets higher might go unnoticed by central banks.

But a stronger economy, higher earnings and emerging inflation pressures could only be ignored by central banks for so long.

Emergency measures would eventually have to expire — and it seems we are nearing the time.

In Australia the central bank seems reluctant to remove the punch bowl too soon, choosing instead to almost outsource timing to the US Fed.

Australia will not be first to move to completely remove Quantitative Easing or to eventually raise rates.

But markets are correct in thinking the day draws closer.

The Reserve Bank is sticking with 2024 — but is likely to hit its inflation target of 2.5% long before then.

Find out about

Pendal’s Income and Fixed Interest funds

We are growing in confidence that ongoing supply constraints in our economy will see us hit 2.5% inflation next year.

The RBA will want to see several prints, but 2023 should see the start of a modest hiking cycle.

The expiry of the Term Funding Facility will also have an impact in 2023 and 2024 — that alone pushes mortgage rates up 0.75%.

So the RBA should only need to raise cash to 1.25% by 2024 to see an overall real economy rate structure 2% higher.

At that point the punch bowl will be gone and the party will end.

Let’s hope people taking on large amounts of debt today can cope.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

In all the investor excitement about AI equities, investors may be missing a crucial factor. Pendal equities analyst ELISE MCKAY explains

- Generative AI capturing investor imagination

- But high electricity costs could hinder usage

- Find out about Pendal Horizon Sustainable Australian Share Fund

- Find out about Pendal Focus Australian Share Fund

Big US tech stocks are soaring on a wave of new, advanced AI applications.

But similar to Bitcoin’s early days, excited AI investors may be overlooking the technology’s extremely high power costs and potential associated sustainability issues, argues Pendal Aussie equities analyst Elise McKay.

While the remarkable progress of AI promises to revolutionise industries, the sheer cost of the electricity needed to train and run the systems puts a question mark over the long-term prospects of adoption.

“There’s three key components of power usage required for running a generative AI model,” says McKay.

“First of all, there’s the power needed to simply build the equipment that it runs on.

“Then there is the enormous power required to train the model.

“And then every time you ask it a question it requires new computations — and that means more power.”

Even before generative AI became widely available, demand for data was expected to increase at a compound annual growth rate of 40 per cent per year.

The data centre industry is already estimated to account for about 1 per cent of global energy demand, says McKay.

“Just because it’s on your phone doesn’t mean it’s not in a data centre somewhere — and data centres need electricity. Any new technology just increases demand for power.”

McKay uses the example of bitcoin mining, which rapidly increased its share of global energy consumption from next to nothing to an estimated 0.5 per cent in 2021.

“Emerging technologies like bitcoin mining can see very rapid adoption and dramatic increases in demand for power,” says McKay.

“We are now seeing the broad take up of generative AI, which is significantly more power hungry than existing technologies.”

A study by Stanford found that training the popular GPT-3 generative AI system contributed almost 10 times the emissions that the average car consumes in its lifetime, says McKay.

Estimates are the newer GPT-4 model was eight times more power intensive again, she says.

“And you don’t just do this once, you do it regularly.”

Find out about

Pendal Horizon Sustainable Australian Share Fund

OpenAI — the company behind ChatGPT — says it continuously improves its AI model by “training on the conversations people have with it”.

“And each model can only do one search at a time,” says McKay. “So, if 100,000 people search for something at the exact same time you need 100,000 copies of the model otherwise queries will be queued.

“Estimates are that every time you query ChatGPT, it is 300 times more expensive than a Google search.”

High power usage has also raised question marks over the carbon footprint of the technology industry, with many providers shifting to renewable energy to minimise their impact on the environment.

“The high cost of providing AI will hinder its adoption,” says McKay.

“It may mean that only companies willing to pay a high price will be able to use it. There’s a good use case for companies willing to pay for it because it improves productivity, but will we see broad adoption for low-paying use cases?”

About Elise McKay and Pendal Australian share funds

Elise is an investment analyst with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies.

She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

Pendal Horizon Sustainable Australian Share Fund is a concentrated portfolio aligned with the transition to a more sustainable, future economy.

Pendal Focus Australian Share Fund is a high-conviction equity fund with a 16-year track record of strong performance in a range of market conditions. The Fund is rated at the highest level by Lonsec, Morningstar and Zenith.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.