What are the implications for investors from this week’s RBA statement? Where might Dr Lowe go next? Pendal’s ANNA HONG explains

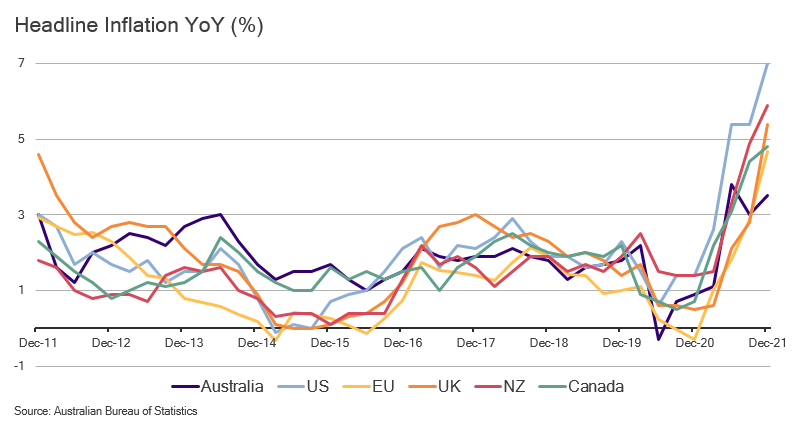

ON A global scale, the picture looks pretty clear — inflation is here.

Here is a comparison of year-on-year headline inflation growth:

- United States 7%

- United Kingdom 5.4%

- Eurozone 4.7%

- Canada 4.8%

- New Zealand 5.9%

- Australia 3.5%

Australian inflation appears modest in comparison to other regions.

But after the RBA has repeatedly reiterated a target inflation band of 2% to 3%, the market is understandably confused.

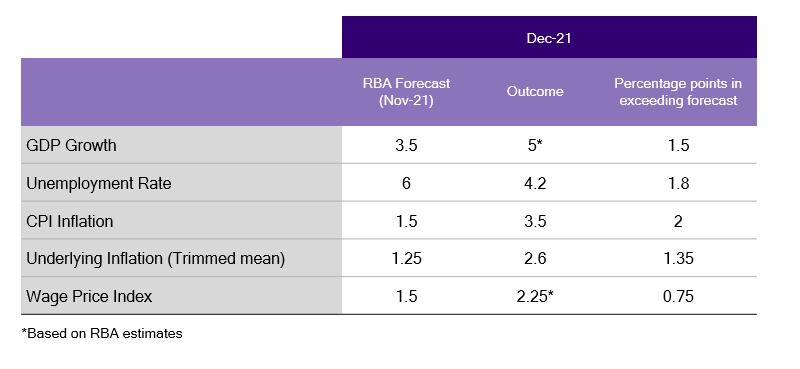

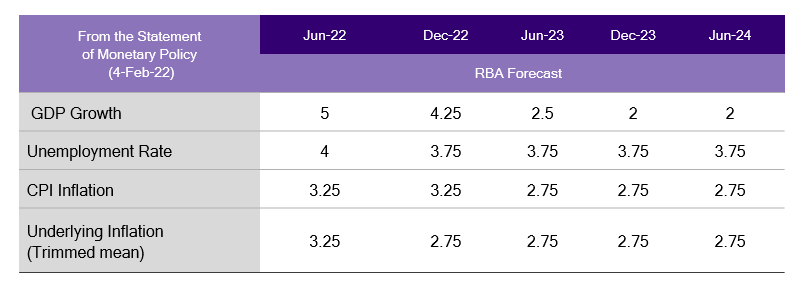

As you can see below, actual data for Q4 2021 exceeded that target — and the RBA is forecasting inflation in the higher part of the target range through to 2024.

Yet the Reserve is saying “no rate hike in the near-term”.

Never before has the RBA been so wrong, so quickly.

This week the central bank was forced to revise its February forecasts to match the market since the data showed that the market was correct.

That led to a stand-off on Tuesday after the RBA statement. The front end of the yield curve rallied but without commitment. Yes, lower for just a bit longer…wait, but how much longer?

The RBA provided a few breadcrumbs for the market to follow.

Dr Lowe’s National Press Club speech made it clear the Reserve was not working off “a specific definition as to what ‘sustainably in the target range’ means”.

It will depend instead on the rate, trajectory, outlook, and drivers of the inflation. In a nutshell – it will be all be about wages.

Why do wages keep Dr Lowe up at night?

In the past 10 years wages growth alongside goods prices have been the main reasons inflation stayed below target.

The RBA appears to be pre-empting the dampening effects of the border re-opening.

It remains worried about the impact on wages if the number of temporary visa holders returns to the pre-pandemic levels. See graphs below.

What are the implications?

The RBA’s preparedness to miss the Q1 and probably Q2 global rate hike party, means conditions for mortgage holders, share markets and owners of short bonds remain supportive.

The picture for long bonds is less clear.

We expect real rates to rise in the months ahead, which is very likely to move nominal yields higher as well.

About Anna Hong and Pendal’s Income and Fixed Interest team

Anna Hong is an assistant portfolio manager with Pendal’s Income and Fixed Interest team.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, the team oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal Sustainable Balanced Fund – Class R (APIR: BTA0122AU, ARSN: 637 429 237)

On 3 February 2022, the existing units of the Pendal Sustainable Balanced Fund (Fund) were reclassified as ‘Pendal Sustainable Balanced Fund – Class R’. The name of the Fund did not change and there were no changes to the terms of the class or your rights as an investor.

What do you need to do?

No action is required. You will be able to continue to invest or withdraw from the Fund.

An updated Product Disclosure Statement (PDS) was issued on 3 February 2022 and made available on www.pendalgroup.com.

The Reserve Bank of Australia has confirmed its shift from hawk to dove — and savers will be going further backwards, says Pendal’s TIM HEXT

FOR most of modern inflation targeting, introduced in 1993, the RBA has leaned on the hawkish side — quick to hike when inflation loomed, slower to cut when it fell.

For years inflation languished below 2% and rates were slowly and reluctantly reduced.

However Covid has brought about a major reset at the RBA.

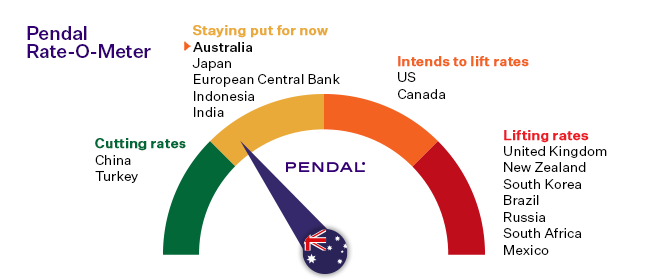

The Reserve is now possibly the most dovish of the developed market central banks and seems prepared to be one of the few to sit out inflation-led hikes.

Then again, they might argue Australia’s 3.5% inflation (in the US it has been nudging 7%) means there is less need for speed here.

The February statement did see the RBA cut its losses on some woefully low inflation forecasts.

The Reserve now expects underlying inflation to be 3.25% this year and 2.75% in 2023.

Unemployment is expected below 4% this year… we are likely almost there now. Full employment is here.

With these new forecasts you may be forgiven for thinking the RBA would conclude inflation was sustainably within its 2-3% band. Well think again.

Referring to inflation at the end of the statement, the RBA says it’s “too early to conclude that it is sustainably within the target band”.

Everyone stand down, time is on our side.

They then cite wages and supply side problems as items to watch in 2022.

Find out about

Pendal’s Income and Fixed Interest funds

Clearly having been so wrong in recent forecasts, they are loathe to jump on board now.

Having only recently assured everyone rates weren’t likely to move in 2022, they don’t want to do a sharp turn.

But what we can really conclude is that the RBA is happy to sit out global rate hikes for now — and certainly doesn’t feel it is behind the curve.

Time will tell.

It’s great news for mortgage holders, share markets and holders of short bonds.

It’s more mixed for long bonds.

Not great news for the AUD. And definitely not great news for savers who are going backwards, seeing prices go up by 3% a year but savings flat-line.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Pendal Fixed Interest Fund (APIR: RFA0813AU ARSN: 159 605 811)

Reduction in management costs from March 1, 2022.

With effect from March 1, 2022, management costs for Pendal Fixed Interest Fund will reduce from an issuer fee of 0.50% pa to 0.45% pa.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

LAST week’s Fed statement was bland, but the press conference that followed was not.

Fed chair Jerome Powell did not deliver a soothing message and the more hawkish tone of his comments raised market expectations around monetary tightening.

The bond yield curve flattened, the US dollar rallied and the US equity market fell in response. However a rebound on Friday saw the S&P 500 finish the week up 0.8%.

The Australian equity market rode the same wave, with the additional distortion of BHP’s index re-weighting exaggerating swings. The S&P/ASX 300 ended down 2.8%.

We remain cautious in the near term. The withdrawal of liquidity combined with the Fed’s aim of slowing economic growth suggests there may yet be more downside.

But we also expect markets to be punctuated by sharp bounce backs as we saw on Friday. This is partly because selling is amplified by the effect of investor hedging, which then unwinds.

It’s important to keep a close watch on the trifecta of rates, oil prices and the US dollar. When all three are rising it usually means a stiff headwind for equities.

However the underlying growth environment remains strong and supportive of earnings. The selling has also been largely indiscriminate, ultimately driving good alpha opportunities.

The Fed’s hawkish message

Chair Powell struck a hawkish tone in his press conference, prompting a sell-off in two-year notes and a flattening of the yield curve. His key messages were:

- This tightening cycle is very different to the last one in 2018. Back then higher rates quickly led to a slump in economic activity and the need for a swift “pivot”. This time inflation is higher, the employment market tighter and the economy stronger. As a result more tightening will be needed.

- The risk is to the upside in terms of the Fed’s inflation expectations.

- The prospect of rate rises is “live” at every meeting this year. This could imply more than the four hikes previously expected.

- The Fed remains data dependent. This has been a consistent message, but the nuance is that their bias is now towards tightening. They would need to see sufficient evidence of slowing to change tack.

- Rates will be the primary tool for tightening. There had been some debate that quantitative tightening would play a larger role to help manage the risk of an inverted yield curve. But the Fed is now clearly saying it needs to see rates higher.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

The market has moved to price in five hikes in response.

The March, May, June, September and December meetings are expected to yield rate rises. At this point the market expects quantitative tightening to begin at the July meeting, while the November meeting coincides with mid-term elections.

The market suspects there will be evidence of a slowing economy or inflation (or both) by that point.

The market is not used to such frequent hiking. But this should be considered in the context of the very low starting point and the fact that monetary policy is still likely to be stimulatory until we go beyond a 2% rate.

The Fed’s goal is to stop stimulating an economy that does not require it. It is looking to get rates back to a “neutral” setting of 2% to 2.5% and shrink the balance sheet from US$9 trillion to US$6 trillion (it was US$3 trillion pre-pandemic).

The essential question – and driver of current uncertainty – is whether this will to be too much tightening or insufficient to achieve the Fed’s aim.

One way to consider this is that the risk balance is asymmetrical.

Higher inflation is considered to be a greater problem than over-tightening, since it would de-anchor inflation expectations and could require a recession for resolution.

It would also condemn Powell and the board to history as the team that lost control of inflation after four decades.

Given this, the goal outlined above is the point at which the Fed will believe they are not making the inflation problem any worse. If it transpires that they have over-tightened and the economy slows too much, they can quickly fall back and pivot as they did in January 2019.

The upshot is that the “Fed put” that helped underpin market confidence has shifted.

The market was conditioned to expect a soothing message from the Fed after equities fell some 10%. Now the perception seems to be that it would take something closer to a 20% fall and widening credit spreads to prompt Fed intervention.

This shift in perception changes the mindset of the market.

The impact of rates on the economy

One of the key questions is how quickly rate rises would affect the economy.

There is a view that the high degree of leverage means small rate increases will affect the economy quickly. But as Chair Powell detailed, this cycle is different to the last. Specifically:

- US household leverage is much lower

- Banks are better capitalised and loan growth is picking up

- There is still a lot of surplus liquidity

- Employment and wages are stronger, supporting income growth

Academic analysis suggests that when you net off the negative for borrowers with the positive for savers, the impact of rates is very mild and only kicks in with a lag.

The impact on investment intentions is also likely to be minimal. Lower rates did not trigger substantially more investment and higher rates are unlikely to choke it off.

There is plenty to underpin a resilient outlook for business investment.

Sustainable and

Responsible Investments

Fund Manager of the Year

This includes the transition away from carbon, good pricing power, the need for more resilient supply chains, the need to deal with labour shortages and the effect of technology on business models.

The areas where tightening may have a disproportionate impact are sentiment and access to capital.

Aggregate financial conditions – how loose or tight an environment is – include not just the level of rates, but also money supply, equity markets, credit spreads, the US dollar and energy prices.

With the US dollar and oil rising as equities fall, we have already seen a meaningful tightening in financial conditions. In time this will begin flowing through to the real economy.

That said, we suspect pent-up Covid demand, the need for inventory re-build and tight labour markets will mean growth and inflation are more resilient.

Conditions also remain relatively loose in a historical context, compared to where we have been over the past decade.

Australian outlook

Australia had its own wake-up call with worse-than-expected quarterly inflation numbers.

The RBA’s preferred trimmed mean measure hit the middle of the 2% to 3% target band two years ahead of forecast.

Since rents, grocery items and new housing prices are all rising and supply constraints remain, it is hard to see inflation easing back.

Wage growth is running at just above 2% and the RBA believes wages rising more than 3% are necessary to be consistent with inflation staying in the target band.

Given the rigid Australian labour market, wages should be slower to rise than in the US, possibly giving the RBA cover to delay a rate hike beyond the market’s expectation of May.

That said, surveys indicate labour shortages and with unemployment falling and higher headline inflation, it is likely we will see wages move higher and the RBA raise rates.

As flagged last week, Australia is in a better place than the US in terms of the need to tighten. Inflation and wages are lower and we didn’t have the same degree of stimulus last year.

Australia is also among the more defensive equity markets at this stage of the cycle, given:

- The market composition is better suited to rising rates, with more financials and resources and less long-duration tech

- A lower valuation

- Less need for tightening

- A weaker currency

How Covid is impacting investors

Australian Covid-related mortality rates are at a high point, but the trend in new cases and hospitalisations is beginning to turn downwards. This is also the case in the UK and US.

In the latter, case numbers are down in 45 states. This is coinciding with evidence that retail and travel activity is beginning to pick up again following largely self-imposed lockdowns.

European cases are on the rise again.

Denmark, which was early into the Omicron wave, has seen a re-acceleration led by the Omicron Ba.2 sub-variant.

Early assessments suggest this sub-variant is about 1.5 times more transmissible than Omicron, but no more severe.

The UK has not seen a surge in the sub-variant yet. But if Denmark proves to be a lead for other countries, it will reinforce the disruption to the economy and supply chains.

Market outlook

The last leg of the US sell-off came with very high volumes, which signalled a degree of short-term capitulation as investors de-risked following a 7% drop.

Measures of the proportion of stocks declining are at extreme levels, suggesting the market may be oversold on a near-term view.

This could indicate a pause in the market, particularly given strength in recent economic data and what should be a constructive US earnings season.

We do not expect a sharp bounce-back at this stage and there is scope for further falls as rates begin to rise. At this point we remain wary of the degree of beta investors will want.

There was an interesting shift in equity markets last week.

As expectations around rates increased, long-duration growth stocks were underperforming. But as the Fed emphasised the goal of slower growth we saw more cyclical sectors hit last week.

In the global tech sector semiconductors had outperformed software by some 40% since October 2021. About a third of that move unwound last week.

Real-time surveys in the US highlight how consumers have become more cautious. Anecdotally this is also true in Australia, which could have a bearing on company outlooks in the upcoming earnings season.

This partly reflects the flattening yield curve but may also signal that the worst of the valuation de-rate in good quality software names is over.

A strong result from Microsoft highlighted strong enterprise demand for software as business models evolve. This is particularly material in the financial sector where the rise of the payment companies has sharpened the focus of banks.

The call between value and growth is more nuanced now.

Value’s outperformance over the past two months is in line with the vaccine-related rebound in late 2020 and early 2021.

But on a long-term basis the relative move still looks muted. Within value we are wary of the more cyclical end due to a backdrop of slowing growth and high leverage as credit spreads widen.

A final interesting observation: this is the first market sell-off to coincide with rising bond yields since the Quantitative Easing era started.

This reinforces the point Powell made about this cycle being different. It goes to the core issue that strategies that have worked in the past 11 years may not work this cycle.

There should be a lot of alpha opportunities in this type of market.

Largely indiscriminate macro-related selling means there has been little differentiation between stocks that are likely to reverse once strong fundamentals become evident, and those that will not.

We have been in a multi-year period where rating has been the dominant driver of returns. There is now the strong possibility that individual company earnings return to the fore.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

What does today’s inflation spike mean for investors? Here’s a quick snapshot from Pendal’s head of government bond strategies TIM HEXT

THIS WEEK’S inflation numbers were extremely strong.

Headline at 1.3% on a quarterly basis and 3.5% annual. Underlying inflation at 1% or 2.6% annual.

Unusually there were almost no negative contributions.

New dwellings, food and fuel were the main drivers but the real surprise came from a wider range of goods which normally see little if any inflation.

Clothing, footwear, furnishings and a wide range of everyday items are going up by around 3 to 5% annually.

Some of that of course is supply related and might come down if things normalise later in the year. But for now that is all speculation.

The RBA once again has been railroaded on its forecasts and will need to address this number in next week’s meeting.

Find out about

Pendal’s Income and Fixed Interest funds

The only thing they can still hang their dovish hat on is wages — but given labour shortages that may move quicker in the year ahead.

Markets actually took the numbers in their stride.

That’s likely because most knew a higher number was a good chance — but also against the current backdrop of risk-off in equities and credit.

Four rate hikes are priced for 2022 with the first in May.

The RBA would have thought that too aggressive, but now may be forced to admit the market has been better at reading the economy.

Although this week’s numbers give support to concerns around inflation, we still don’t expect an unhinging of inflation from the medium term 2% to 3% band.

For investment markets that would not be a bad result.

After all, 2% to 3% is still considered low — and business investment and the economy in general can easily handle that.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

FOUR major issues are influencing markets at the moment:

- Rising rates and the withdrawal of liquidity

- The disruptive effect of the Omicron wave

- The potential for conflict between Russia and Ukraine

- Chinese policy easing

Of these, only the fourth is positive. As a result we have seen equities weaken in the year to date.

At this point the outlook for rates and inflation is the most important issue.

As the broad equity market has fallen, the growth stocks have underperformed. In the US, the S&P 500 fell 5.7% last week while the NASDAQ was down 7.6%.

The Australian market also fell, but less so given a skew to banks and resources over growth sectors. The S&P/ASX 300 fell 2.9%.

The S&P 500 and NASDAQ broke down through their 200-day moving averages for the first time in the post-March 2020 bull market.

This does not mean the market’s run is over. But it is the first meaningful correction, coinciding with a shift in monetary policy and highlighting the importance that liquidity has played in the Covid era.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

It is a well-understood principle that if rates, oil and the US dollar are all rising, equities are likely to drop. Oil and the US dollar index have been rising for a few months. The move higher in rates has been the final piece.

The Fed’s meeting this week will be an important near-term signal. The market has adopted a very hawkish view on policy in the past three weeks. Some see potential for Quantitative Easing (QA) to end immediately; the risk of an immediate rate hike; or signs that an expected hike in March could be 50bps rather than 25bps.

We think that those moves are unlikely. The Fed may seek to assuage the more hawkish concerns, which could actually see a relief rally.

Despite a sharp sell-down in markets and the possibility of soothing words from the Fed, the underlying challenge of inflation remains.

As a result we do not see this as a time to be re-loading on some of the sold-down names.

Rates outlook

The drop in the overall market and the correction in growth has been caused by two factors: the market moving to price in rates rising to around 2% by end of next year and the realisation that liquidity will start drying up.

The market is considering four broad scenarios:

- The bull case: 2% rates do the job, inflation eases, economic growth slows but remains solid, earnings continue to grow and the market valuation rating holds

- Central banks over-tighten like we saw in 2018 as the pandemic makes gauging the economy hard. The economy and earnings roll over in response and the market sells off.

- Rates continue to rise – possibly above 2% – but this does not derail the economy. This is a traditional scenario similar to the mid-to-late 1990s. Earnings continue to grow, supporting markets and offsetting an equity de-rating

- The bear case: inflation proves persistent. Central banks have to engineer a hard landing to re-anchor expectations. This would hit earnings hard and see markets sell off

The key point is that we are looking at a very disparate outcomes, creating more uncertainty for markets

Inflation outlook

The key underlying question is what will limit and bring down inflation.

This could be a combination of:

- Higher prices choking off demand and slowing the economy, ie inflation curing itself

- Debt and high leverage meaning the economy is sensitive to small rate changes and modest hikes working to bring down demand

- Demographics and aging populations suppressing demand and credit growth

- Technological disruption continuing to act as a deflationary force

On the flip side, arguments for persistent inflation include:

- Excess stimulus continuing to support demand

- Structural decline in labour market supply underpinning wage growth

- Transition to clean energy leading to higher fuel costs and investment spending

- China shifting away from export model to dual circulation

- The policy imperative as governments suppress real rates to manage debt

We don’t know the outcome. But it is clear that inflation presents more an issue today than at any time in the past couple of decades.

Liquidity a significant issue

The withdrawal of liquidity is potentially as significant an issue for equities as the debate around rates.

The shift in the liquidity environment is likely to make this a tougher year for equities. In our view, persistent growth in equities since March 2020 with no material correction is due to the surplus liquidity evident in money supply data.

QA is unwinding faster than expected. US money supply growth has slowed from just shy of 30% per annum at its peak to just above 10% now. This means less surplus liquidity to be funneled into financial assets.

Sustainable and

Responsible Investments

Fund Manager of the Year

Early warnings signals have been evident for some time in the more speculative parts of the market.

Some, such as the ARK Innovation ETF and Chinese tech indices peaked a year ago and are off about 60% since then. Others such as crypto and the solar and IPO ETFs tracked sideways through to October/November and are off 30-50% since then. Tesla and the broader Electric Vehicle and battery sector have proven more resilient, but are showing signs of rolling over.

The overall market has held up better – particularly the growth indices – due to the performance of the mega-caps. But this appeared to be changing last week, as they also started to underperform.

The US earnings season is expected to be decent and could help offset recent weakness. But there have been some disappointments in early results, notably Netflix. There is also risk that the market focuses on near-term uncertainty from Omicron’s disruption.

Credit spreads have not budged. This, along with resilient commodity prices, suggests the market is not yet at the point where it believes policy will derail the cycle.

That said, there is a view that we will need to see credit spreads widen to help tighten financial conditions sufficiently to restrain inflation. In this context, low spreads may not be as unambiguously positive as is usually the case.

It is important to note that the Australian market is more defensive and better protected in this environment due to the index mix. It is also less extended on valuation.

Covid and economic disruption

The good news is that global cases may be peaking.

New daily case data is increasingly convoluted and hard to measure. US waste water analysis suggests this wave was five times the size of the previous one, but is now rolling over.

It is becoming clear that Omicron is less severe than previous strains, though there is no consensus on why.

Regardless, health systems are coping, albeit under a lot of strain. In NSW the proportion of hospitalised patients needing to go into ICU is less than half the previous wave.

Omicron’s sheer transmissibility is still creating a lot of disruption. Some companies have seen more than 30% of their workforce unable to work, leading to businesses effectively shutting down. This is a risk to supply chains, particularly if the strain becomes established in China.

Real-time surveys in the US highlight how consumers have become more cautious. Anecdotally this is also true in Australia, which could have a bearing on company outlooks in the upcoming earnings season.

All that said, the market has tended to look through near-term numbers and we suspect this will continue.

There are signs we are entering the phase of learning to live with Covid. This should help some of the oversold re-opening stocks.

Russia/Ukraine threat

The odds of a Russian invasion of Ukraine have risen considerably in recent weeks. This adds to market uncertainty and is a risk for energy markets and gas supply. This is an issue to keep watching.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s head of equities Crispin Murray today challenged BHP’s proposal to collapse its dual-listed company (DLC) structure.

“As BHP Ltd (Australia) shareholders, we are not in favour of BHP’s proposal for the collapse of its DLC structure,” Mr Murray said.

On December 8, BHP announced a final board decision to end the DLC structure and unify its corporate structure under the existing Australian parent company, BHP Group Limited.

BHP Group Limited and BHP Group Plc shareholder meetings are expected to take place on January 20 with unification due to be complete by January 31.

“This proposal is transferring value from Australian Limited shareholders to offshore PLC shareholders. This value transfer has been evidenced by the material decline in the Australian multiple of earnings that BHP Ltd trades on,” said Mr Murray, who leads one of the Australia’s biggest Australian equities teams for independent asset manager Pendal Group.

“We appreciate that the main reason for the proposal is the greater flexibility it provides to do large M&A deals in the future. However, there are two questions we have around this. Firstly, BHP has had a poor track record in this regard historically. There is a risk that Australian shareholders pay the price for the unified corporate structure and then see more value destruction overtime. Secondly, while a unified corporate structure will make doing scrip-based M&A easier, the decline in multiple potentially negates this.”

Pendal expects that should the proposal not go through the long-term premium of the Australian listed company to PLC would return.

Below, Mr Murray outlines Pendal’s main issues with the proposal:

What has been the value destruction borne by Australian shareholders to date?

The BHP Ltd share price fell 14% in the two days (17th-18th August 2021) following the announcement of the DLC collapse.

The premium of BHP Ltd’s (ASX) share price to BHP PLC’s (LSE) share price — which had existed almost since the inception of the DLC — fell from more than 20% to around 5% after the announcement.

Even with the more recent recovery in resources, the stock has underperformed the market by about 15%, in line with the reduction in the Ltd premium to PLC.

This premium is likely to erode further if the vote goes through.

In our view, this represents a substantial, permanent and unnecessary value transfer from Australian to PLC shareholders.

BHP management expected the UK share price to re-rate to a multiple in line with the Australian listing.

In fact, the opposite has occurred.

The charts below show the absolute PE of BHP Ltd vs the ASX200 is at a 10-year low, despite the overall rise in market rating.

Relative to industrials, the stock is almost half the rating it was 10 years ago.

If a key motivation is to enable scrip-based M&A, the reduction in multiple makes any potential acquisition less appealing.

Has the dual listed structure impacted BHP’s ability to do M&A?

In our view, none of the reasons BHP is proposing as rationale for the collapse of the DLC structure would stand in the way of BHP executing its strategy.

The DLC structure was consciously put in place by BHP, at its discretion, at the time of the Billiton merger. It has now been in place for 20 years and through this time BHP has had no issue implementing its strategy or accessing capital.

BHP has a strong balance sheet and access to debt and equity capital markets across multiple geographies and listings.

In the preamble to the US Onshore petroleum stake in 2017 — and under activist shareholder pressure — BHP vigorously defended the DLC structure and concluded it was too expensive to unwind.

Most of the costs associated with the DLC collapse have increased in the interim and are expected to be $350mln to $450mln.

But M&A is not always a good thing…

We respect the BHP Board and management. However, we do note how difficult it is to execute effective, large-scale deals in the resources sector.

To highlight this, there are a number of examples of unsuccessful transactions under former BHP management. These include:

- The merger with Billiton. After 15 years, BHP chose to demerge most of the Billiton assets into South 32 (S32), since they did not meet BHP’s standards of being low cost and long life. The demerger resulted in de-rating of the S32 earnings of about 33%, which persists today.

- The 2011 acquisition of PetroHawk and Fayetteville for U$15.1bn and US$4.8bn respectively. An additional US$18.9bn was spent on the assets during ownership. Ultimately these assets were sold for US$10.8bn in FY18 after an attributable EBIT loss of US$5bn during ownership.

- The 2005 acquisition of WMC Resources. This includes Olympic Dam and Nickel West. Neither asset has fulfilled the original expectation of returns.

- There was also the failed attempted acquisition of Potash of Saskatchewan (Canada) in 2011 at a price that subsequently fell away materially.

BHP has had cumulative write-downs of $22.9bn since 2001. Much of this relates to assets bought at too high a price.

M&A in the resource sector is difficult. The likelihood is that value accrues to the acquired company’s shareholders.

That Australian shareholders wear the current value destruction from the collapse of the DLC just to simplify M&A in the future is challenging to accept.

Isn’t this really about the de-merger of the petroleum business?

In our view, reassessment of the DLC structure is tied to the decision to de-merge the petroleum business.

While BHP has stated it would go ahead with the demerger even if the DLC was not collapsed, the company has highlighted that it would make the process simpler.

We believe these two strategic decisions need to be evaluated separately.

And, again, we are not sure it is in the interests of Australian shareholders to accept the value destruction of the DLC collapse for a simpler demerger that may or may not go ahead.

Are there broader implications for the market?

The consolidation of BHP on the ASX will see its ASX 200 index weight rising from about 5.8% to about 9.6%.

While this is not the concern of BHP management, taking a macro view highlights that such a concentration of index weighting is not ideal for Australian broad market investors. It reduces diversification and impacts expected risk-adjusted returns.

It certainly will, however, lead to an increase in ‘non-discretionary holdings’ from index funds and those managing benchmark risk. This could reduce active shareholder pressure on management. We would strongly argue that this is not in the long-term interest of BHP shareholders.

Conclusion

We appreciate the company’s motivation for seeking to collapse the DLC structure in terms of simplifying management of the organisation.

BHP PLC shareholders will also benefit from this one-off gain, though many of those with current PLC stock may not ultimately be long-term holders. This is why there is very little push-back on the proposal.

But in our view, as detailed above, this proposal is clearly not in the interests of Australian BHP Ltd shareholders.

Given the clear value destruction and the questionable benefits accruing from the change, Pendal will be voting shares under its management against the proposal.

Pendal Geared Imputation Fund (APIR: RFA0130AU, ARSN: 102 970 089)

Pendal Imputation Fund (APIR: RFA0103AU, ARSN: 089 614 693)

Pendal MidCap Fund (APIR: BTA0313AU, ARSN: 130 466 581)

AFTER 35 years in the industry and 24 years with Pendal, Andrew Waddington will retire at the end of March 2022.

Andrew leaves with the gratitude and best wishes of Pendal and recognition of the contributions he has made to the success of Pendal’s Australian equity franchise.

Andrew will hand management of the Pendal Midcap Fund to Brenton Saunders from April 1, 2022.

Brenton has been with Pendal for nine years as a research analyst in the resource sector and portfolio manager of the BT Natural Resources Fund.

He has a total of 28 years of experience including 25 as an analyst and 16 as a portfolio manager.

Brenton will commence as Co-PM of the Fund with Andrew Waddington from January 7.

There will be a period of transition as Brenton takes greater ownership, before he becomes the sole portfolio manager after Andrew’s retirement at the end of March.

Brenton’s depth of experience, long tenure with the team, extremely strong performance record as portfolio manager and his close collaboration with other Pendal portfolio managers leaves him placed well to continue the Pendal Midcap Fund’s success.

The Pendal Imputation Fund and Tax Effective Funds, which Andrew co-managed, will be solely managed by Jim Taylor from January 7, 2022. He will be supported by Oliver Renton.

There have been no updates to the Funds’ Product Disclosure Statements (PDSs) or Target Market Determinations (TMDs) which can be found at pendalgroup.com.

Here are the main factors driving the ASX this week according to our head of equities Crispin Murray. Reported by portfolio specialist Chris Adams.

Find out about Crispin’s Pendal Focus Australian Share Fund

Find out about Crispin’s sustainable Pendal Horizon Fund

This is the final weekly note from Pendal’s Australian equities team for 2022. We wish our clients and readers a well-deserved rest after a very busy year. Our weekly note will return early in the new year.

COVID and inflation have been the two big issues to watch all year. Both have taken significant turns in recent weeks, leaving the outlook for 2022 as uncertain as ever.

This does not mean that the outlook is necessarily negative.

Rather, the potential paths we head down next year look very different:

- On Covid: We could be in the early phases of the largest wave. This could put substantial strain on healthcare systems, prompting renewed restrictions which could drag on the economy and escalate supply chain problems.

Alternatively we may discover the effects of the vaccines, anti-virals and potential lower virulence of Omicron mean the virus becomes more benign — to be handled without restrictions.

- On inflation and rates: We could see economic strength and a tight labour market sustain inflationary pressures. This could prompt both the Fed and markets to realise that higher real rates are needed, prompting a sell-off in equities and growth stocks in particular.

Alternatively, we may see inflationary pressures ease as supply chains resolve themselves, people re-enter the labour force and structural factors such as tech and debt re-assert. In this scenario growth and earnings are good and we see bonds and equities rallying, with growth resuming leadership.

Now is not the time for betting the house on one of these directions.

We should have a far better understanding of the Omicron issue within three weeks, while the rates issue will take much of next year to play out.

Our portfolios are low on thematic risk. Instead we are looking for features such as good cash flow, strong stock-specific stories and good franchise strength.

We are maintaining a tilt to re-opening plays given the poor sentiment right now. But we are mindful of the near-term path, given the potential for more negative short-term news flow.

Markets were down last week. The S&P/ASX 300 fell 0.7% and the S&P 500 lost 1.9%.

Pendal Focus Australian Share Fund

Now rated at the highest level by Lonsec, Morningstar and Zenith

Concerns about central bank policy and the degree to which rates need to rise to contain inflation weighed. So too did uncertainty over Covid due to contradictory research on Omicron risks and increasing government restrictions heading into Christmas.

Covid and vaccines outlook

Surging case numbers in a number of countries — notably the UK and Denmark — are fanning concerns about healthcare systems coming under strain.

The interplay between Delta and Omicron waves is complicating an assessment of the situation and government reactions. For example The Netherlands has reimposed lockdowns despite material falls in new cases, fearing that an Omicron wave will see new cases hurtle higher again.

The risk of Omicron breakthrough infections — ie vaccinated people catching the virus — is 5.4x higher than it was for Delta, according to research from the Imperial College in London.

The key question concerns the disconnection between cases and hospitalisations.

South African data is hard to interpret because it is subject to large backward revisions. For example, the number of people in hospital with Omicron was revised up 61%. Many of these patients are in hospital for other reasons and have incidentally tested positive. This is leading some to conclude that there have been far more asymptomatic cases than first thought.

The number of new daily cases in Gauteng Province — home to more than a quarter of South Africa’s population — is falling.

This has happened within a month of the wave’s start — rather than the usual two to three months in previous waves.

There are a number of theories to explain this:

- Case numbers are being significantly understated due to a higher proportion of asymptomatic cases

- Changes in social behaviour — people self-isolating more quickly — may have a containing effect

- Better medical treatment

- A portion of the community is not susceptible to the variant

- A significant portion of the population is transient and has left the province as we approach Christmas

Each of these explanations have quite different interpretations.

The other issue is a disconnection with hospitalisations. Does this reflect lower severity or is it a function of the younger demographics in Gauteng?

A study from Imperial College — not yet peer-reviewed — claims there is no reason mutations in Omicron should lead to less severity. If there are lower case numbers it is because of vaccinations, the study says.

Nevertheless, the proportion of people needing critical care — as well as the length of hospitalisations — are materially lower than the last wave. This suggests there is some factor helping reduce severity.

Covid in the UK and US

The UK will provide an acid test. It is too early to draw conclusions on hospitalisation rates. But we are seeing a high incidence of positive tests among British patients hospitalised for other reasons. This suggests a high rate of asymptomatic cases.

The UK will provide the lead for US, which will be the key driver of market sentiment.

US cases overall are still not rising quickly. They are up 3% week-on-week. But this was held down by declining numbers in the Midwest. Lead indicators suggest a material acceleration with the New York testing positivity rate doubling in three days.

The most effective response to Omicron is the third jab. This reloads the number of immune antibodies, materially reducing risk of breakthrough infection.

The case growth has triggered an acceleration of boosters in most affected countries, though capacity to administer shots at this time of year is constrained.

Sustainable and

Responsible Investments

Fund Manager of the Year

The key issue for markets is the policy response to this wave of cases.

The near-term risk is that markets fear the worst and governments feel the need to act, reimposing restrictions. We are already seeing this come through with US Q4 GDP forecasts moderating to 6%, down from 7-8%.

This could see a sentiment-driven sell-off in markets. But it is important to note the strength of nominal GDP growth, which means earnings should remain firm.

Economics and policy

The Fed came in at the hawkish end of the expected range, doubling the rate of Quantitative Easing tapering. QE should now end in March. The Fed’s “dot points” now indicate three hikes in 2022.

The market was initially positive because there was no escalation of inflation concerns. It is worth noting that the expected terminal value of rates did not budge, remaining at 2.1% by the end of 2024.

There are two disconnections worth noting.

First, the market does not currently believe the Fed will need to raise rates in 2023. It sees rates peaking around 1.5%, reflecting confidence in inflation fixing itself.

Second, the Fed and the market both believe inflation can be fixed without real rates ever going positive.

There is a school of thought that believes this is not credible because of key differences between this cycle and previous examples:

- Household balance sheets are far stronger

- Fiscal stimulus is far greater

- The degree of QE has been much higher

- Changes to the labour market and supply chains

- The impact of greenflation

- Real rates have been far lower for longer

There are small signs that the Fed’s pivot is already prompting inflation expectations to moderate and that we may have passed through peak fear on this front.

There are also signals that people are returning to the labour market in the US, with the participation rate edging up.

Outside the US, the Bank of England raised rates from 0.1% to 0.25%, surprising a market that expected them to hold steady given the risk from Covid. This was seen as a negative, suggesting the BOE sees inflation as a key risk.

The ECB was more balanced, announcing the end of its pandemic program of QE but putting in place a transition program. This is designed to prevent fears that early rate rises put peripheral bond markets under pressure. Inflation is less of an issue in the EU currently, which gives them more latitude.

US fiscal policy took a twist today with Senator Joe Manchin announcing he will not support the current Build Back Better package in its current form.

This likely means the current model, which was to put in programs for one, three and five year periods to reduce their apparent cost, is dead.

Rather Biden will need to reduce the programs he wants to commit to and ensure they are fully funded. This still looks likely, given Manchin’s relationship with Biden. But it will take time and will be a set-back for renewable energy-related stocks.

Markets

Overall we believe the market environment is still reasonably constructive.

Growth is strong, companies have pricing power, rates remain very low and sentiment is not over-confident.

In the near term the Covid case spike could hold the market back. The early read on Omicron suggests any further sell-off would be an opportunity for bombed-out cyclicals.

The medium term issue is that the market seems to be underestimating the policy response required to contain inflation.

In this environment a focus on higher-returning, good-quality franchise positions is an important part of the portfolio.

It is also worth noting the continued rebound in iron ore.

This is partly driven by inventory re-stocking, but also reflects improved sentiment on China. Beijing continues to signal a more pro-growth policy shift, albeit with no major stimulus yet announced.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.