Markets are around fair value, economic data is contradictory and market momentum is patchy — so it’s a good time to be close to neutral, argues Pendal’s MICHAEL BLAYNEY. But be ready for opportuities

- Inflation still high but moderating

- US rates likely to rise another 50 basis points

- Investors should be neutral in equities and bonds

- Find out about Pendal’s multi-asset funds

INTEREST rates are set to rise again after this week’s US CPI figures, though the data shows some heat is coming out of inflation.

The January headline rate of inflation in the US was 6.4 per cent higher than a year earlier. Core inflation was up 5.6 per cent.

It was “pretty much as expected”, says Pendal’s head of multi-asset Michael Blayney. “Inflation is too high but it’s coming down.”

How should investors react?

“There are always risks,” says Blayney. “It’s a natural feature of the economic/market cycle. Inflation, interest rates, earnings and the potential for a recession are all in focus.

“For investors, that means sticking to their plan.

“Markets are fair value at the moment and it’s a good time to be a bit like Switzerland – neutral. It’s time to be patient and wait for an opportunity.”

Market expectations matter

While the absolute CPI numbers matter, markets tend to react relative to expectations, notes Blayney.

Find out about

Pendal Multi-Asset Funds

Market reaction to this week’s CPI print was relatively muted.

“For the market, it’s not what the number is,” says Blayney. “It’s what the number is relative to what the market expected.”

“The US inflation figures reinforce the high probability of a 25-basis point hike to 5 per cent in March.

“But it doesn’t change the overall picture of high-but-moderating inflation.

Futures markets are implying the Fed Funds rate will peak around 5.25 per cent mid-year.”

Inflation will fall before rates

One difference this cycle is that the Fed will be determined to see inflation falling before cutting interest rates – having learnt from past experiences, Blayney says.

He notes that market volatility after an inflation print or Fed rates decision has lessened in recent months.

“Those factors remain very important, but markets have shifted their attention somewhat to recessionary risks and corporate earnings.”

Recession outlook

In terms of recessionary risks, Blayney says leading indicators have been weakening over the past year, though there has been a small bounce recently.

“They’re still bad, but less bad – and that usually makes markets reasonably happy.”

And while corporate earnings have been downgraded, things aren’t as poor as first feared.

Blayney adds a caveat: “Historically spikes in inflation and the related Fed hiking cycles have flowed through to earnings with a lag.”

Another factor is Pendal’s in-house market stress indicator, which has been falling for a number of months as markets start to see a turning point for inflation.

Finally, China reopening, and Europe emerging from winter much better than expected in economic terms, has mitigated global recession risks.

Where to look for opportunties

Blayney says it’s a good time for investors to be Switzerland – neutral.

“Markets are around fair value. Economic data is contradictory and market momentum is patchy so it’s a good time to be close to neutral.

“But there are still some reasonable relative value opportunities.

“For example in equities, small caps all around the world are cheap relative to large caps. In the US for example, small and mid-caps as a percentage of market cap are near 20-year lows.

“That doesn’t necessarily mean they outperform in the short term if there is a recession, but it does mean they have a great set-up for the next decade.”

Bond holdings should be around investors’ strategic long-term level.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

“They will still be helpful in the case of a recession, and are now generating much better yields,” Blayney says.

“It’s hard to make a compelling case for credit at the moment given spreads have shrunk. Right now you simply aren’t paid well to take on credit risk.”

Stay diverse

As always, it’s about having a diversified portfolio, Blayney says.

“You need to own some assets that will do well if growth is better than expected, like equities, and some assets that will do better in a recession, like bonds.

“And you should hold some assets with cash flows that are indexed to, or resilient to, higher inflation.

If market pricing is wrong and there’s persistent inflation, investors are going to want this because historically inflation has tended to be bad for earnings and bad for bonds.”

About Pendal’s multi-asset capabilities

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

These include Australian and international shares, property securities, fixed interest, cash investments and alternatives.

In March 2024, Perpetual Group brought together the Pendal and Perpetual multi-asset teams under the leadership of Michael O’Dea.

The newly expanded nine-strong team will manage more than $6 billion in AUM and create a platform with the scale and resources to deliver leading multi-asset solutions for clients.

Michael is a highly experienced investor with more than 23 years industry experience, including almost a decade leading the team at Perpetual.

Find out more about Pendal’s multi asset funds

Contact a Pendal account manager here

This is an archived article.

In 2024, Perpetual Group brought together the Pendal and Perpetual multi-asset teams under the leadership of Michael O’Dea.

Michael is a highly experienced investor with more than two decades of industry experience, including a decade leading the team at Perpetual.

The newly expanded team provides a platform with the scale and resources to deliver leading multi-asset solutions for clients.

You can find out more information about the changes here.

Don’t be fooled by the allure of higher term-deposit rates – you can do better, says our head of cash strategies STEVE CAMPBELL

IT’S a bad take on Amy Winehouse, but ‘no, no, no’ is bang-on when it comes to investing in term deposits right now.

The TD question is increasingly coming up as the Reserve Bank moves closer to pausing monetary policy tightening.

In early 2022, after being starved for yields over an extended period, investors were awestruck with the 1%+ yields on offer for 12-18-month tenors.

At the time it looked great.

I doubt those who locked in are feeling so happy now about the decision to tie liquidity up in a lower yielding asset.

We can expect the Reserve Bank to hike rates twice more in the near term, taking the cash rate to 3.85%.

Find out about

Pendal’s

cash funds

For vanilla cash funds, we expect a return in the 4.1% to 4.3% range and higher again in Pendal Short Term Income Securities Fund.

Yes, our vanilla cash funds and the Short Term Income Securities Fund do carry other risks compared to term deposits including a higher credit risk.

Term deposits up to $250,000 carry a government guarantee under the Financial Claims Scheme, something that our funds do not benefit from. Widening credit spreads can also detract performance on the Short Term Income Securities Fund.

The advantage? Access to liquidity on a same-day or t+1 basis.

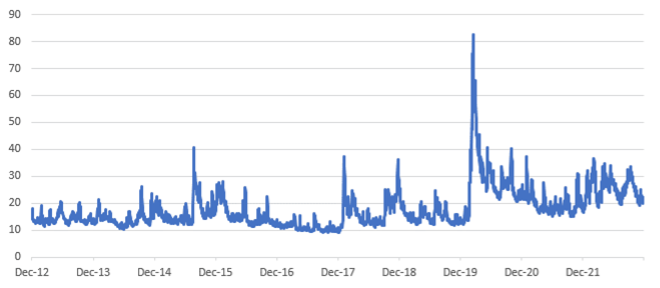

Last year we had no lack of volatility in financial markets, as shown by the VIX index below:

This year may not be as volatile, but I doubt calm waters lay ahead for the rest of 2023.

The effect of large monetary policy tightening is still to be felt.

Inflation has proved to be more persistent than expected. Labour markets continue to surprise globally with their recent strength.

In this environment why lock up liquidity in a term deposit?

The marginal return is not that different to highly liquid funds and TDs can only be broken in extreme circumstances – none of which anyone wants to experience.

Higher liquidity is something that should be increasingly valued in the year ahead.

TDs? No, no, no.

About Steve Campbell and Pendal’s Income and Fixed Interest team

Steve Campbell is Pendal’s head of cash strategies. With a background in cash and dealing, Steve brings more than 20 years of financial markets experience to our institutional managed cash portfolio.

Find out more about Pendal’s cash funds:

Short Term Income Securities Fund

Pendal Stable Cash Plus Fund

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

The RBA today tightened monetary policy by another 25 basis points, with the promise of more to come. Pendal’s STEVE CAMPBELL explains what it means for investors

THOSE looking for the Reserve Bank to provide some respite from higher rates will be left disappointed after today’s decision and hawkish accompanying statement.

The RBA tightened monetary policy by a further 25 basis points to 3.35%, with the promise of more to come.

Ahead of updated economic forecasts later this week, the RBA today revealed some of its projections including:

- Headline inflation falling to 4.75% in 2023 and 3% by mid-2025

- Economic growth dropping to 1.5% over 2023 and 2024. The post-Covid spending spree that benefitted growth in 2022 has run its course, buffers have been drawn down and economic growth will suffer

- Unemployment forecast to increase to 3.75% by the end of 2023 and 4.5% by mid-2025. The labour market remains tight, though there are signs these pressures are easing slightly

The statement concluded with: “The Board expects that further increases in interest rates will be needed over the months ahead…

“…In assessing how much further interest rates need to increase, the Board will be paying close attention to developments in the global economy, trends in household spending and the outlook for inflation and the labour market.

“The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that.”

The December-quarter inflation data released in late January exceeded the RBA’s expectations and clearly has it concerned.

The market now has a follow-up hike of 25 basis points priced in at around 70% probability and a full hike priced in for April.

The terminal cash rate is now priced at almost 4% later this year.

Inflation remains the priority

The market had been looking for a softer statement, perhaps following the lead of other central banks recently.

Two weeks ago The Bank of Canada explicitly stated it would pause on policy action as it assessed “the impact of the cumulative interest rate increases”.

The European Central Bank and Bank of England both tightened policy by 50 basis points, but delivered statements that saw yields rally further out the curve.

In the US, the Federal Reserve delivered a 25 basis point hike. The market priced the terminal peak as almost reached — until the “wow” non-farm payroll number and better-than-expected ISM services data released last Friday.

Find out about

Pendal’s

cash funds

The RBA is more than aware of the risks posed by the fixed rate mortgage cliff from the middle of the year.

But inflation remains its priority in the near term. Until it heads south they will be on tenterhooks.

The lack of a monthly inflation data series with a long history does the RBA no favours.

The next quarterly inflation release is not due til late April.

The next key releases in February are the labour and wage price index data due on the 16th and 22nd.

Consumption data from retail sales — along with consumer confidence — will also be closely watched.

What it means for investors

With higher yields and steeper curves in the short end of the curve, investors will benefit from their cash portfolios returning closer to 4% in the coming months.

I keep getting questions about investing in term deposits.

Why do this in a rising interest rate environment — in a period where volatility is elevated?

Cash funds offer comparable returns but provide liquidity. It can be quicker to sell a house and get your money rather than waiting for a term deposit to mature.

About Steve Campbell and Pendal’s Income and Fixed Interest team

Steve Campbell is Pendal’s head of cash strategies. With a background in cash and dealing, Steve brings more than 20 years of financial markets experience to our institutional managed cash portfolio.

Find out more about Pendal’s cash funds:

Short Term Income Securities Fund

Pendal Stable Cash Plus Fund

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

If the US falls into recession, investors should be ready to buy falling equities and take advantage of higher bond yields, says Pendal’s head of multi-asset MICHAEL BLAYNEY

- US economy likely to fall into recession

- Investors should be ready for opportunities

- Find out about Pendal’s multi-asset funds

IT’S probable the US Fed’s rate hikes will push the world’s biggest economy into recession this year.

“Some of the forward-looking indicators in the US like the ISM’s Purchasing Managers Index are showing signs of weakness,” says Blayney.

“There have also been some broker earnings downgrades, though history tells us that the more significant downgrades tend to happen after the event.

“Overall, this has been one of the most forecast US recessions ever.”

How should investors respond?

How to invest in a recession

Sticking to a long-term strategy is critical, Blayney says, though at the edges there is room to move.

That means holding a little more cash than usual, he says.

Find out about

Pendal Multi-Asset Funds

“At this point it pays to be a little cautious, so we are a little underweight US equities.

“Last year the most important thing was to be underweight both bonds and equities in aggregate.

“At present we prefer taking relative value positions since markets are much less expensive than they were, effectively pricing in some of the bad news.

“While we are underweight the US, we maintain overweights to some of the cheaper, more ‘value’ equity markets like Australia and the UK.”

Investors should have some “dry powder” ready to use if valuations fall as a result of a recession, Blayney says.

“If the US goes through a recession and earnings are hit and markets fall, there will be an opportunity to buy equities. Markets do tend to over-react – both when times are good and when times are bad.”

Bonds look reasonable

Bond yields are now at “reasonable” levels, Blayney says.

The critical point is when the US Fed stops lifting interest rates, and potentially changes course and starts cutting.

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

“If there is a recession, having some bonds in a portfolio will be a good thing because the Fed will have to step back from lifting rates.

“But it’s likely the Fed will want to make sure inflation is beaten before moving to cut rates.”

“In terms of momentum, the trend has been against bonds even if their valuations are now okay.

“But the cycle is turning a little bit towards government bonds in the sense that the economy is weakening.

“We are still slightly underweight, but I think government bonds are now reasonable value.

“If you look at corporate bonds, they got a bit cheaper last year.

“But credit spreads have come in as equity markets have risen. So compared to government bonds, corporate bonds are not offering great regward for risk if there’s a recession on the way.”

It’s not about forecasting recession

Good portfolio construction is not necessarily about trying to forecast recessions, Blayney says.

“It’s about maintaining balance, having a long-term strategy, at times dialling down the risk, and at other times dialling up the risk.”

Why bonds, why now

Ausbiz’s Nadine Blayney interviews CBA chief economist Stephen Halmarick and Pendal head of bonds Tim Hext

ON-DEMAND WEBINAR

About Pendal’s multi-asset capabilities

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

These include Australian and international shares, property securities, fixed interest, cash investments and alternatives.

In March 2024, Perpetual Group brought together the Pendal and Perpetual multi-asset teams under the leadership of Michael O’Dea.

The newly expanded nine-strong team will manage more than $6 billion in AUM and create a platform with the scale and resources to deliver leading multi-asset solutions for clients.

Michael is a highly experienced investor with more than 23 years industry experience, including almost a decade leading the team at Perpetual.

Inflation data due in January will set the scene for another rate hike in February. But from there the pace should slow, says Pendal’s head of cash strategies STEVE CAMPBELL

THIS week’s 25-point rate rise probably won’t be the last — but the Reserve Bank’s pace of tightening is likely to move from monthly to quarterly increments next year.

The cash rate will now sit at 3.1% for the summer. The RBA’s next monetary policy statement is due on February 10.

Between now and then we will see fourth quarter inflation data released on January 25.

It will be high. The annual headline inflation rate will be around 8% for 2022.

This will set the case for another hike in February.

Tuesday’s RBA statement contained nothing new. The central bank remains data dependent while the global outlook has deteriorated.

Domestically the labour market remains tight. Economic growth has been strong and household spending will start to slow due to policy tightening delivered so far.

For some this is yet to occur, given the higher-than-usual number of fixed-rate mortgages that are yet to reset.

This is the reason why the RBA doesn’t need to be as aggressive. Fixed-rate mortgages at rates around 2% will be resetting closer to 5.5% mid next year.

The RBA acknowledges they are walking a tight rope.

Find out about

Pendal’s

cash funds

“The path to achieving the needed decline in inflation and achieving a soft landing for the economy remains a narrow one.”

The further they push policy, the harder the landing becomes.

The RBA doesn’t want to cause a recession. But given a choice of embedded higher-inflation expectations or better growth, the former wins out for any central banker.

The longer-term task is no simpler.

Policy action to date “has been necessary to ensure that the current period of high inflation is only temporary”, the RBA statement said. “High inflation damages our economy and makes life more difficult for people.”

In a speech late last month RBA governor Phil Lowe pointed out that variability in inflation outcomes was more likely to increase than what we’ve become accustomed to.

He cited four key areas where supply issues in the longer term will occur:

- Reversal of globalisation

- Demographics

- Climate change

- The energy transition in the global economy.

The RBA has under-shot or over-shot its 2-3% target band more often than not over the past 15 years.

More variability in inflation outcomes? Who would want to be a central banker.

Central banks have tightened policy significantly over 2022 — and that will weigh on demand over 2023.

The current Christmas spendathon — where we are let loose for the first Christmas in three years — will hold activity up for now. But it’s unlikely continue into the new year hangover.

The supply side of the global economy is also likely to see capacity increase and downward inflationary pressure next year.

The supply issues that have resulted from the pandemic and Russia’s invasion of Ukraine will resolve over time.

But with it comes another set of challenges. And those are more likely to be skewed towards higher inflationary pressure in the longer term.

About Steve Campbell and Pendal’s Income and Fixed Interest team

Steve Campbell is Pendal’s head of cash strategies. With a background in cash and dealing, Steve brings more than 20 years of financial markets experience to our institutional managed cash portfolio.

Find out more about Pendal’s cash funds:

Short Term Income Securities Fund

Pendal Stable Cash Plus Fund

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

An annual strategic asset allocation review has led Pendal’s multi-asset team to make some recent adjustments to portfolios. Pendal’s ALAN POLLEY explains

- Strategic asset allocation process takes a long-term view

- Key factors are renewable energy, higher inflation and geo-political risk

- Find out about Pendal’s multi asset funds

THE build-out of renewable energy infrastructure, persistent higher inflation and geo-political risk will characterise investment markets in coming years.

But the threat of low returns related to zero interest rates is in the past as central banks revert monetary policy to more normal levels.

These are some of the findings from an annual strategic asset allocation review by Pendal’s multi-asset team.

“The strategic asset allocation process is where you forget about the day-to-day noise and think about the long term,” says Alan Polley (pictured below), a portfolio manager with the team.

“Investing, by definition, is long term. But we all get caught up in short-term, random happenings that tend to get averaged out over the long term.

“The strategic asset allocation process is that annual time to think about the long-term investment views, how you’re thinking about markets and asset classes and how to get the best outcome for your investors over their investment time horizon.”

Six major, long-term themes

Polley says six secular themes will likely characterise investment markets in coming years:

- The ongoing importance of ESG themes (from a risk and opportunities perspective)

- Better productivity

- Ageing demographics

- High debt and deleveraging

- Enhanced geo-political risk

- Higher inflation and spike risk

“One of the secular themes we have dropped this year is the risk of a low-return world.

Find out about

Pendal

Multi-Asset

Funds

“For the past decade everyone’s been talking about expected investment returns being low.

“The main reason was because central banks had pushed down real rates to negative and market valuations to stretched levels.

“But that’s normalised. Cash and real rates are at reasonable levels.

“And now that markets have sold off as well, forward-looking returns are looking pretty good — probably the best they have for a decade.”

The other risk that is no longer hanging over markets is the prospect of a shock from the withdrawal of easy monetary policy.

“It’s been difficult this calendar year, but rates normalisation has effectively occurred.”

Inflation risk remains

Remaining as a risk is inflation, which will be a theme investors have to deal with for some time, says Polley.

“Investors consume real assets and so they’re interested in real returns. Over the last decade you’ve had this tug of war between deflation and inflation.

“Inflation will be higher than it was in the last decade and central banks are more likely to achieve their inflation objectives (as opposed to undershooting them).

“But we also think there’s more chance of inflation spikes.”

Portfolio adjustments

Weighing up the themes has led the multi-asset team to make some adjustments to portfolios.

“We’re increasing our exposure to bonds. They are offering attractive yields and have material diversification benefits again.

“This will also help defend against a potentially more volatile long-term outlook with more geo-political risk and less-supportive central banks.

“Another change we’ve made is moving some capital into listed, sustainable listed investment companies. With the secular theme of higher inflation, you want more real assets.

“The way we’re looking to get that real asset exposure is via renewable and sustainable companies with underlying real assets.”

Emerging Markets risk

“The other major change is we’re reducing exposure to emerging markets. The emerging markets index has a very high exposure to China that’s increased materially over the years to circa 30 per cent.

“Taiwan is another 15 per cent in emerging markets — so if there’s conflict, that’s almost half of the emerging markets index at risk.”

“China also appears to be transitioning to more authoritarian and nationalistic policies at the expense of market-based reforms.

Compounded by increased global national security concerns and politically driven onshoring preferences, deglobalisation could reduce China’s global manufacturing dominance. “

About Alan Polley and Pendal’s Multi-Asset capabilities

Alan is a portfolio manager with Pendal’s multi-asset team.

He has extensive investment management and consulting experience. Prior to joining Pendal in 2017, Alan was a senior manager at TCorp with responsibility for developing TCorp’s strategic and dynamic asset allocation processes covering $80 billion in assets.

Alan holds a Masters of Quantitative Finance, Bachelor of Business (Finance) and Bachelor of Science (Applied Physics) from the University of Technology, Sydney and is a CFA Charterholder.

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

There are three steps in checking the health of an investment portfolio. Pendal multi-asset portfolio manager ALAN POLLEY explains

- Annual asset allocation review critical to successful investing

- Three steps: strategic asset allocation, active asset allocation and diversification

- Find out about Pendal’s multi asset funds

A REGULAR portfolio health check is a critical part of successful investing — doubly so after a volatile 2023.

But what’s the right way to conduct a check up on your portfolio?

There are three parts to a successful annual portfolio review says Alan Polley, a portfolio manager in Pendal’s multi-asset team.

Here’s a quick snapshot.

1. Review strategic asset allocation

The first and most important step is reviewing your strategic asset allocation — in other words checking he long-term investment strategy is still consistent with your return objectives and risk tolerance, says Polley.

“It’s been a tough year. Equities and bonds are both down around 15 per cent this year.

“Some people may feel like their portfolio construction process is broken. But that’s where you come back to your long-term strategic plan.

It’s important to keep in mind the long-term returns from staying invested.

“Markets go up and down and you get paid through the cycle for those ups and downs.

“Since 1900, the average equity real return is around 5.4 per cent a year for developed markets, and a good per cent higher for Australia and the US.

“There were all sorts of global events and wars in there. But you got that return by keeping your long-term strategy consistent with your risk tolerance and your annual return objectives.”

Sound economic rationale

There is a sound economic rationale why this is true. Financial markets should pay a risk premium to people who choose to put their money at risk by investing, instead of keeping their savings safe in cash.

The strategic asset allocation part of a portfolio review is about adjusting your portfolio to ensure it still matches your long terms goals, risk tolerance and investment return objectives.

“Your risk tolerance changes naturally over time as you age, and potentially other exogenous life events,” says Polley.

“As you get older, you simply have less time left to recover from drawdowns, so you need a more capital stable portfolio. At some point, you will also need more income.”

Find out about

Pendal

Multi-Asset

Funds

But your risk tolerance and long-term goals are not changed by a negative year on the markets, says Polley.

“When markets are volatile, your portfolio can stray away from your risk tolerance, either to a more defensive or aggressive position and potentially at the wrong time.

“The point of the strategic asset allocation process is to provide a sound central portfolio that enables you to rebalance, buying cheaper assets and selling more expensive ones.

“Buying cheaper asset classes at lower prices — the ones that have sold off and are giving you the pain — should add to your returns over time. As should selling the more expensive assets.”

2. Consider active asset allocation

Overlaid on the strategic asset allocation process is a review of your active asset allocation.

“This is where you can make short-and-medium-term asset allocations around your strategic asset allocation to enhance returns.

“This is what we refer to as going overweight or underweight relative to the strategic asset allocation.”

Active asset allocation changes the risk profile of a portfolio slightly — but the incremental additional gains can compound over a lifetime into a significant difference at retirement.

Polley says there are two keys to successful active asset allocation.

The first is having the discipline to ensure the active positions in a portfolio average out over the course of a cycle to match the overall risk objectives.

“If you go overweight, you should at some point also go underweight such that sum of those overweight and underweight positions is zero — which means the average allocation along the cycle is equal to your strategic asset allocation.”

The second is ensuring that your active position sizes are modest compared to your strategic asset allocation.

“The sizing of an active allocation should be roughly up to 10 per cent the sizing of the strategic asset allocation because it’s the strategic asset allocation that is calibrated to meet the investor’s return and risk objectives over time.

“Active allocations need to be incremental because we don’t want them to put us off the path of the optimal long-term portfolio and the portfolio’s targeted risk tolerance.”

The complexity and discipline required to successfully manage active tilts in a portfolio is why many investors choose to use professional fund managers for this portion of their investments, says Polley.

3. Ensure sufficient diversification

The final step in a portfolio health check is ensuring you have sufficient diversification.

“It’s often said — but tends to be forgotten — that diversification is the only free source of return in investing. So when you think about your strategic asset allocation, really try to maximise the level of diversification in your portfolio.

“That means having non-traditional assets alongside your traditional assets.

“Non-traditional assets should at least hold their value like they have this year when traditional assets fall and that gives you the dry powder to sell and rebalance.

“The benefits of rebalancing doesn’t work if all your asset classes fall at the same time.

“You need something that holds value or better yet performs at different times to traditional assets — cash holds its value and non-traditional assets almost by definition perform at different times.”

About Alan Polley and Pendal’s Multi-Asset capabilities

Alan is a portfolio manager with Pendal’s multi-asset team.

He has extensive investment management and consulting experience. Prior to joining Pendal in 2017, Alan was a senior manager at TCorp with responsibility for developing TCorp’s strategic and dynamic asset allocation processes covering $80 billion in assets.

Alan holds a Masters of Quantitative Finance, Bachelor of Business (Finance) and Bachelor of Science (Applied Physics) from the University of Technology, Sydney and is a CFA Charterholder.

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

The long-term outlook for investment markets is more positive than it has been since 2014, argues Pendal’s Alan Polley

- Bonds attractive once again

- ‘Long-term opportunity set looks better than it has been for a while’

- Find out about Pendal’s multi asset funds

THE long-term outlook for investors is more positive than it has been for almost a decade, giving reason for optimism despite the volatility of 2022, says Pendal’s Alan Polley.

The forecast comes from Pendal’s multi-asset team, which has just completed its annual strategic asset-allocation process, looking at long-term trends and expected returns across asset classes.

Key to the forecast is improved returns for bonds. US 10-year treasury yields have risen almost 3 percentage points in 12 months, offering attractive yields for the first time since the global financial crisis.

Bonds can once again play a defensive role in a traditional balanced portfolio — often termed a 70:30 portfolio for its split between equities and fixed income — as well provide a reasonable level income.

This is even more important for conservative portfolios, which tend to have a higher allocation to bonds.

“The investment outlook now is more normal than it has been for a decade,” says Polley, a portfolio manager in the multi-asset team.

The 70:30 portfolio is not dead

“Over the past five or so years there’s been commentary declaring the death of the 70:30 portfolio.

“Not only was it never dead, but now it’s definitely back and in a much stronger position than it has been for quite some time.”

That’s a good thing for investors, says Polley.

A significant implication of low returns over the past decade has been a move by investors up the risk curve into private markets and illiquid assets. Many saw no alternative.

“Looking forward, you’d think the marginal dollar that’s been chasing illiquid assets will start to dissipate, and this issue will be compounded with lagged higher discount rates.”

Investors looking for clues from history as to how markets will perform should look back to the 90s and early 2000s — because the ultra-easy monetary policy distortions of the post-GFC world are over.

“We’re going back decades prior to the GFC for a reference point when central banks weren’t artificially manipulating markets with low cash rates and quantitative easing.”

Find out about

Pendal

Multi-Asset

Funds

Lift in long-term returns

Across all asset classes, Pendal’s review shows forward-looking, long-term returns have lifted about 1.5 per cent on average from last year.

“That additional 1.5 per cent really increases the chances of a portfolio achieving its return objectives.”

The multi-asset team’s strategic asset allocation process is run annually to analyse long term investment market behaviours.

“It’s important because all investors have a return objective and risk tolerance. The strategic asset allocation process is about building an optimal portfolio that meets those risk tolerances and long-term return objectives.

“Over the long term, what really determines your outcome is your risk tolerance, which leads to whether you invest in a 70:30 fund or a 30:70 fund or 90:10 fund.

“This is where having a long-term perspective matters,” says Polley.

“The whole point of investing is that over the long term, through the cycle, you expect to get paid for incurring the short-term ups and downs.

“You need to stay the course with a long-term investment strategy that’s consistent with your risk tolerance.

“Right now, because central banks have been materially unwinding their exceptionally loose monetary policy and markets have sold off and become better value, the long-term opportunity set is looking better than it has been for a while.”

Sustainable and

Responsible Investments

Fund Manager of the Year

About Alan Polley and Pendal’s Multi-Asset capabilities

Alan is a portfolio manager with Pendal’s multi-asset team.

He has extensive investment management and consulting experience. Prior to joining Pendal in 2017, Alan was a senior manager at TCorp with responsibility for developing TCorp’s strategic and dynamic asset allocation processes covering $80 billion in assets.

Alan holds a Masters of Quantitative Finance, Bachelor of Business (Finance) and Bachelor of Science (Applied Physics) from the University of Technology, Sydney and is a CFA Charterholder.

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

Trend, valuations and the economy are the key measures when deciding if it’s time to re-enter the market, says MICHAEL BLAYNEY

- Bond, equities closer to fair value

- Opportunity to rebalance portfolios

- Find out about Pendal’s multi-asset strategies

MANY investors are trying to pick the right time to re-enter the market.

Pendal’s multi-asset chief Michael Blayney is closely watching three key market drivers – the trend, valuations and the economic and earnings backdrop.

“The history of markets tells us that often when it gets to fair value, markets fall through that level and that’s when there are great buying opportunities,” says Blayney.

“It’s when the newspaper headlines say it looks diabolical. We’re not quite there yet but…”

Three key things drive markets, says Blayney.

1. The trend

“There’s the trend. That’s the tendency of markets that have been going up to keep going up, and those that have been going down to keep going down. That tends to work over shorter time horizons.

2. Valuation

“Then there’s valuation. Through time, markets do tend to revert to some sort of measure of fair value.

“Ultimately markets are real companies generating earnings that have value, and people are willing to pay for that over time and through the cycle.

“Over the long term, there’s a sensible range, and when [assets] get outside of that range, they have a habit of coming back in.

Find out about

Pendal Multi-Asset Funds

3. Economy

“The final thing important to the market is the economic and earnings backdrop. That essentially provides the subjective overlay.”

Time to invest?

On these three critical measures, it’s time to start inching back into some markets, Blayney says.

“The trend is still negative, though there’s been some short-term bounces. The trend measures we look at say we’re still very much in a bear market in equities and bonds.

“On the value side, we’re now at the point where we think in aggregate, equities and bonds are fair value,” Blayney says.

Though a regime-shift from a falling and low interest rate environment to a rising rate environment complicates the analysis, he says.

“It kind of reminds me of the kids in the back seat of the car always asking, ‘are we there yet’? Well, we might be there in terms of fair value.”

Adviser Sam is invested

in making our world

A better place.

Watch as Sam meets a

mum rebuilding her life

thanks to responsible

investing

That doesn’t mean that market won’t fall further because investors tend to overshoot on the downside, Blayney adds. But they do ultimately revert.

Consider fixed income

Fixed income valuations across geographies, with some notable exceptions, seem reasonable, Blayney says.

“Australians bond and US treasuries are both around our estimates for fair value.”

Fixed income is a critical part of the valuation puzzle because other assets classes are valued in relation to bond yields.

“We’ve just updated our long-term capital market assumptions and for the first time in a long time, things look sensible.

“You’ve got cash at a sensible level. You’ve got bonds at a decent premium to that and then equities on top.

“It’s been a painful adjustment, but we’ve gotten to the point where, at least for the long-term investor, it’s a pretty reasonable point to be back in the bond market.”

What about the economy?

The third factor driving markets is the economic cycle and company earnings.

So far in this US September quarter profit season, positive surprises have been slightly lower than other quarters.

“But when you buy a stock, you are buying earnings into the distant future. From a valuation measures, the earnings cycle is normalising,” Blayney says, adding that investors should be focusing on relative value positions.

“We like the Aussie market, the UK, Japan and markets with weaker currencies that could support earnings,” he explains.

“We are still underweight the US and Europe.

“Europe has quite a diabolical backdrop with energy, high inflation, high debt levels — and the single currency makes them a little bit less flexible.

Three-legged stool

“The market is like a three-legged stool,” says Blayney.

“Right now, value has improved. It’s telling you be neutral.

“The trend is still negative and that’s telling you to be underweight.

“And the cycle is still negative, but we are getting more clarity on that.

“Investors need to be vigilant.”

About Pendal’s multi-asset capabilities

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

These include Australian and international shares, property securities, fixed interest, cash investments and alternatives.

In March 2024, Perpetual Group brought together the Pendal and Perpetual multi-asset teams under the leadership of Michael O’Dea.

The newly expanded nine-strong team will manage more than $6 billion in AUM and create a platform with the scale and resources to deliver leading multi-asset solutions for clients.

Michael is a highly experienced investor with more than 23 years industry experience, including almost a decade leading the team at Perpetual.

Australians should prepare for another 25-point rate hike next month before policy tightening slows in the new year, says Pendal’s head of cash strategies STEVE CAMPBELL

THE US Fed hiked rates overnight by 75 basis points to 4 per cent, but indicated that future hikes may occur in smaller increments.

The key line here was: “the committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments”.

The market has priced in a terminal rate (essentially the peak of the Fed’s interest-rate cycle) of just over 5 per cent by the middle of next year.

As expected, the Fed remains open to more aggressive moves to tame inflation if needed.

What it means for Aussies

The Reserve Bank of Australia is a couple of months ahead of the Fed when it comes to the cumulative tightening effect.

In early September Governor Phil Lowe dropped a hint that the pace of tightening would slow when he said “the case for a slower pace of increase in interest rates becomes stronger as the level of the cash rate rises”.

The RBA followed through with its decision to tighten less than expected in October when raising the cash rate by 25 basis points.

Find out about

Pendal’s

cash funds

The decision to increase the cash rate by a further 25 points to 2.85 per cent on Melbourne Cup Day was in line with expectations.

What of the RBA’s decision?

Most had been expecting a 25-point move this month, in line with the RBA’s move last month.

A higher-than-expected third-quarter inflation number prompted headlines that 50 basis points was a possibility.

The market had assigning about a 20% chance of that.

Consequently, short-dated bank bill futures rallied after the announcement, though volumes were very light.

The RBA revealed some of the economic forecasts that will be included in Friday’s monetary policy statement.

These include:

- Inflation is now forecast to peak at around 8 per cent later this year, from up 7.75% previously

- CPI inflation is expected at around 4.75 per cent over 2023 and just above 3 per cent over 2024

- Economic growth around 3% for 2022, 1.5% for 2023 and 2024

- Unemployment rate to remain around the current 3.5% before rising to over 4% in 2024 as the economy slows

What’s next?

Further rate increases are expected, according to the RBA.

Key uncertainties remain on the response of household spending to monetary policy tightening and a gloomier global economic outlook.

We believe another 25-point hike is more likely than not in December.

Next year should see things change however, with policy tightening likely limited to one or two hikes.

For many race-goers Tuesday was a tough day. That’s also the case for households with a variable mortgage.

For households with fixed-rate mortgages mid-2023 and beyond is when the pain is really set to kick in with mortgages repayments about to increase sharply.

The RBA is more than aware of this. It’s a reason not to overtighten in the first half of 2023.

About Steve Campbell and Pendal’s Income and Fixed Interest team

Steve Campbell is Pendal’s head of cash strategies. With a background in cash and dealing, Steve brings more than 20 years of financial markets experience to our institutional managed cash portfolio.

Find out more about Pendal’s cash funds:

Short Term Income Securities Fund

Pendal Stable Cash Plus Fund

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.