In this short video, Pendal’s Income and Fixed Interest team outline the expertise, diversity of thought and disciplined decision-making processes that drive outcomes for clients

An excerpt from the team’s interview

Pendal’s Income and Fixed Interest team bring together deep experience, specialised knowledge and a collaborative structure that help set it apart in the market.

In this video, the four lead portfolio managers — Amy Xie Patrick, Tim Hext, Steve Campbell and George Bishay — explain the advantages of specialisation.

“We don’t want people covering too much – true expertise takes time and depth,” says Tim Hext, head of government bond strategies.

“We focus on depth, and we back that with strong quantitative models and real-world insight from markets, central banks and beyond.”

Pendal maintains a unified approach to cash, credit, income and government bond strategies which encourages richer discussions and stronger risk awareness.

“We’re constantly cross-pollinating ideas,” says Steve Campbell, head of cash strategies. “Every portfolio decision benefits from diverse perspectives and a shared understanding of risk.”

Further supporting this model is the team’s top-down process, which George Bishay – head of credit and sustainable strategies – says blends quantitative modelling with real-world experience and market insight.

“It’s this combination that helps us actively manage risk and seize opportunity,” he says.

Whether supporting institutions, advisers or individual investors, the Income and Fixed Interest team prioritises strategic thinking, active risk management and – importantly – strong client partnership.

“From sovereign wealth funds to everyday investors, we work hard to understand each client’s needs and help them build stronger portfolios for the long term,” says Amy Xie Patrick, head of income strategies.

Get to know our portfolio managers better in these individual profile videos:

Find out about

Pendal’s Income and Fixed Interest funds

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

In this video profile, Pendal’s head of government bond strategies TIM HEXT explains why the case for bonds – and active management – has never been stronger

An excerpt from Tim’s interview

In this video, Tim Hext – head of government bond strategies at Pendal – shares insights drawn from a 30-year career spanning trading desks, bank balance sheets and state government funding.

His deep understanding of both the macro conditions and inner workings of bond markets have helped shape the strategy behind the Pendal Government Bond Fund.

Tim explains how Pendal’s active management approach can help capture value beyond the macroeconomic view, through the skillful selection of securities from across the government bond universe.

“Even in volatile conditions, government bonds give investors the flexibility to respond – to rebalance, or to lean into opportunity,” he says.

“We position for where the economy is going – not where it’s been – and we go deep on security selection. Knowing how different states fund and price their debt helps us capture opportunities others miss.”

Watch the video to learn more about Tim and Pendal’s active approach to fixed-income investing.

Get to know the rest of the team better in these individual profile videos:

Find out about

Pendal’s Income and Fixed Interest funds

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Cast back to the year 1998 when Paul Wimborne, co-manager of the Pendal Global Emerging Market Opportunities Fund started looking at Emerging Markets, and the world was a different place: the US was impeaching its President, Argentina was heading towards default and we had a big tech bubble forming on the NASDAQ with unsustainable returns, and of course the Australian cricket team retained The Ashes. Unprecedented times indeed!

But consider the structure of today’s emerging markets and its clear there have been some more permanent changes. Emerging economies are a fairly disparate group, with many barely recognisable to the asset class that existed in the 1990s and 2000s, where a crisis in one particular market usually spread rampantly across many others.

In the past three decades, many of these countries have embarked on monetary and fiscal reforms, building defences against such external shocks. This difference was evident through the past year when the US dollar strengthened, prompting investors to exit emerging markets. Countries with these policy defences escaped relatively unscathed, while others like Argentina and Turkey showed their vulnerability.

Leading investment research firms like Lonsec argue that today’s emerging markets warrant a dedicated place in an overall global equity portfolio. While emerging markets only represent around 10% of the MSCI All-Country World global share index, they are materially underrepresented based on their true share of the global economy. Today, emerging markets account for 59% of global GDP. There are now more than 120 companies that have joined the Fortune 500 which are facing into emerging markets.

So why does this discrepancy in recognition persist? There are a few reasons but the prime explanation is found in the underlying structure of share market indices. They are generally based on market capital weightings, which essentially represents the total value of a company’s shares on issue. Take the global technology behemoths for example — Apple, Microsoft, Google and Amazon — their collective representation in the index accounts for around 8% of the developed markets index, not far from the total index weight of all emerging markets.

Valuations now attractive

China epitomises the extent of this discrepancy. Despite its status as the world’s second-largest economy, China is still defined as an emerging market due to low household income levels, which are just 15% of what they are in the United States.

“Valuations look attractive, even in spite of trade wars …”

Veronica Klaus, Head of Investment Consulting, Lonsec

And the US-China trade war and associated rhetoric has played its part in driving lacklustre returns from emerging markets in recent years, leading many investors to write off the asset class.

“Valuations look attractive, even in spite of trade wars …” according to Veronica Klaus, Head of Investment Consulting at Lonsec.

Lonsec believes many of the fears are overdone, although this is not a blanket statement to cover all 1,149 stocks in the emerging market index as they’re not without risks. Klaus refers to the volatile nature of parts of the emerging world. For the year to date, Chile’s share market has declined by 7%, while Russia is up 32%, precisely why Lonsec impresses upon the importance of active management for the asset class.

Lonsec argue for an active, selective approach to emerging markets for clients with a long term growth horizon. Klaus says “What is important is to look for active management, and look to a manager and a strategy that is moving away from these higher risk scenarios and looking towards the long term valuation opportunities.”

Lonsec sees value stocks within emerging markets as being particularly cheap, “trading at their largest discount since December 2001”.

“It’s much more attractive compared to US shares and Australian bonds.”

Lonsec holds an overweight stance in emerging markets across their suite of balanced or growth oriented model portfolios.

Click here to download the complete article

Importance of the country’s business model

Paul Wimborne, co-manager of the Fund concurs on the point of being selective. We are not compelled to buy any stock; regardless of what is or isn’t in the benchmark, the investment has to measure up on our country-level macro assessment and the bottom-up fundamentals of a company.

“The key question you have to ask yourself is, do I want to be invested in that country…or not?”

Paul Wimborne, Senior Fund Manager

We don’t say bottom-up analysis isn’t important in emerging markets, but we are very different to the conventional approach. Our bottom up analysis recognises that the key factors we put into our company analysis models are actually top-down in nature. Our process is inherently designed to reflect the belief that emerging markets go right or wrong at the country level.

Take Argentina’s 45% stock market crash in August this year; it didn’t matter if you were in the best Argentinian company that day. The business model of that company is not going to help you out. “The key question you have to ask yourself is, do I want to be invested in that country…or not?”

In emerging markets there are always countries that go wrong. We need to satisfy ourselves with regard to what we like about the macroeconomic environment that means the equity market is going to do well. Then we find the companies that will benefit from the macroeconomic environment and avoid companies that are susceptible. It is vital to understand the country’s operating model in all of its guises, as it is intricately linked to the success of a company.

Unlike in the developed world where there is a greater degree of synchronicity in economic factors between countries, emerging markets feature a much more diverse group. Variables like GDP, interest rates, inflation, regulation, cost of capital and terminal growth rates can be materially different and much less correlated relative to developed markets.

When will emerging markets turn?

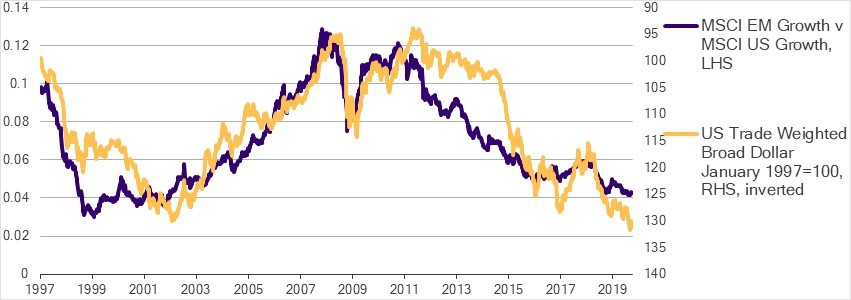

Our team believes there are two key conditions conducive to delivering strong performance in emerging markets: robust global growth and a weak US dollar. Clearly neither of those factors are in place – and until they are the team are being very selective and taking advantage of idiosyncratic opportunities in the asset class.

We do think the second of these catalysts may come through. When that does happen we should see emerging markets begin to outperform developed markets, in keeping with their historical relationship.

Weaker dollar to drive EM recovery

Source: Pendal, Bloomberg as at 4 October 2019

The rationale for this to occur at some point is fairly clear. First, the US dollar retains its reserve currency status. This means the US can borrow lots of money at cheap rates, and they are certainly borrowing plenty and driving up the deficit. Heading into the US election year, all signs are there for whoever takes office, that spending will all but continue and add to the deficit. The question will be who is going to finance the fiscal deficit? Over the last few years it has been the Fed and sovereign investors like China that have been buying US treasuries and adding to their expansive reserves.

Evidence is now emerging that China is increasingly moving to price commodity contracts outside of the US dollar payments system. At the margin, this means there is less rationale for holding all of your reserve assets in US dollars. So if it’s not foreigners buying as many US treasuries, and it’s not China or the Fed, who will be financing the deficit?

Evidence from prior crises shows that typically when currencies blow out, it’s driven by financing of enlarged fiscal deficits. When they can’t get foreigners to finance it, the Government turns to the local banking sector and you get a crowding-out effect. Essentially this means the banking sector becomes constrained with less money to lend to the domestic economy. The recent spike in US repo rates may have something to do with this dynamic.

When and how this happens can’t be predicted with certainty, but when it does we’re likely to see growth-focused investors switch preferences from NASDAQ tech stocks to emerging markets. But until this occurs we remain focused on country-specific, self-help opportunities through countries like India, Korea and Turkey.

The team believes India has the strongest growth potential over the next few years. Among the many differentiators, it is one of the only countries in the world which hasn’t had an increase in the credit-to-GDP ratio since 2008.

One reason is a number of loans made in the banking system went bad prior to 2008. The Modhi-led Government has made a concerted effort to redress shortcomings of the previous Bankruptcy Code. They have strengthened the banking sector with fresh capital and we should see a credit-driven recovery for the banking sector. There has been a delay in this cycle as credit growth has fallen in response to the collapse of a non-bank lender. However, we believe the recovery should eventuate, bolstered by a series of other reforms implemented under the Modhi Government.

Then there’s Korea, a very different opportunity. Korea has been one of the cheapest markets historically, largely due to its poor governance record. This is changing as political and social pressure is driving different behaviour in the ‘chaebol’ conglomerates which dominate Korea’s corporate landscape. One key, tangible benefit is an increase in payout ratios, helping lift Korea’s traditionally poor dividend yield. We see this trend continuing, which will likely lead to a substantial re-rating of Korean equities and potentially, its eventual graduation into the developed markets category.

Source: MSCI, Bloomberg as at 31 December 2018. Free cashflow is cashflow from operations less capex

Other bright spots in the emerging market world are Russia, Mexico and Turkey — all for very specific reasons. Turkey serves as an example of how quickly conditions can turn positive. With 2019 GDP growth revisions of -1.5%, Turkey was until recently the second-weakest of all emerging economies this year. However, the pricing of that forecast slowdown became wildly excessive, and the Turkish stocks we bought in May have outperformed substantially. Interestingly, Turkey’s 2019 GDP growth estimate has since been revised upwards, suggesting that the worst of the selling pressure (and the greatest opportunity for investing) was right before the turn in May.

These and other examples serve to validate our view that success in emerging markets relies on a balanced assessment of fundamentals and valuation. We look to use both to identify top-down, country-level opportunities in emerging markets, irrespective of how good or bad the global environment is perceived or otherwise at that moment. We see the key macro catalysts for re-rating as likely as conditions in the global economy evolve. When they do arrive, it will likely add to success for our country-specific investment decisions.

We think the challenges and opportunities in emerging markets underpin the importance of our country-driven approach. We continue to identify opportunities — such as those discussed — which exist despite the headwinds to the asset class more broadly. Meanwhile, we monitor the landscape for signs of a change in those headwinds, positioning the portfolio to benefit at the point when the tailwinds return to emerging markets.